Business Valuation – Income Approach

07 May, by

Business Valuation – Income Approach

1. Introduction

There are 3 approaches to business valuation, and they are

a) Adjusted net assets approach (Balance Sheet approach)

b) Multiple-based approach (Comparative approach)

i) Based on comparable public-listed company

ii) Based on recent comparable M&A transaction

c) Discounted cashflow-based approach (Income approach)

The Income Approach is by far the most rigorous. But there are computation/technical difficulties in this approach which this article addresses. These are:

a) What is the key concept in the income approach?

b) What is the method of computation of business value using income approach?

c) Understanding the 2-part cashflows (5-year explicit forecast period and terminal value period) to be applied in the approach.

d) Determination of the discount rate or adjusted WACC

e) The perpetuity factor and the Gordon Model

f) Understanding Enterprise Value derived from the Income Approach

g) Deriving Equity Value (EqV) from Enterprise Value (EV)

h) Sensitivity Analysis/Financial Modelling to arrive at an appropriate range of values.

i) Counter-check range of values using the multiple-based or other approaches and reconcile the differences.

2. Concepts in business valuation

The assets in the Balance Sheet as at a specific date (the valuation date) consist of both operating and non-operating assets. The company uses operating assets, not non-operating assets in operations to generate profits and grow the business. As there is a financial limit to growth, sales growth would require additional working capital resources to support. There may also be a need for additional CAPEX, for example, more investment in vehicles to deliver goods. With these investments in place, sales growth can continue into perpetuity, barring unforeseen economic or political disruptions.

The value of the company at valuation date is the discounted cashflows of the operating profits to perpetuity. There are 2 obvious challenges.

a) Adjusting operating profits into after-tax cashflows

b) Dissecting the stream of cashflows to perpetuity into 2 sections viz a defensible 5-year forecast and a terminal value, from 6th year to perpetuity.

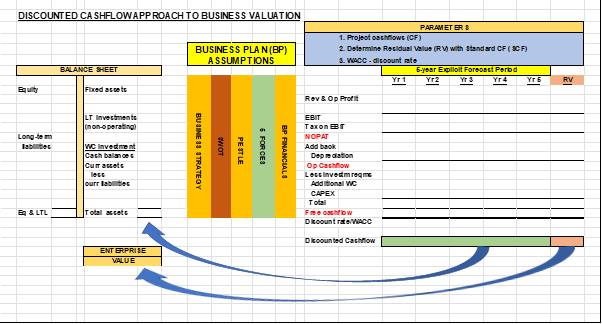

The diagram below shows the flow of economic resources from operating assets as at valuation date to cashflows in perpetuity, based on business plan assumptions.

3. Context of valuation

To understand the process of valuation using the income approach, we need to go back to first principles. The Balance Sheet is a reservoir of assets, liabilities and equity. On the right-hand side of the Balance Sheet are the assets, both operating and non-operating (LT investments). On the left-hand side, are the funding resources, equity and LT liabilities. The operating assets are used in operations to generate profits and cashflows, in perpetuity. With increases in sales and expanded scope of operations, there must be additional working capital (typically inventory) and additional CAPEX to support and fund the growth.

Operating performance is captured in the P&L resulting in operating profit (EBIT) and profit after tax (PAT). But for valuation purposes, we must capitalise cashflows (not EBIT or PAT) to its present value (at date of valuation), using a discount rate, which is typically the WACC.

For operating assets to generate a stream of operating profits and cashflows, there must be a defensible business plan. In some cases, an extended 3-year budget (to 5 years) is used, which may not be adequate as valuation will not be defensibly maximised.

4. Operating profits and cashflows in perpetuity

To ascertain the value of the entity as at valuation date (say, 31 December 2014), the operating profits and cashflows from 1 January 2015 to perpetuity must be decomposed into 2 manageable periods, viz

a) a 5-year explicit forecast period (2015 TO 2019), and

b) a terminal or residual period from the beginning of the 6th year (2020) to perpetuity.

The explicit forecast period is normally 5 years. It could be longer, and the test is whether P&L for the end of the period provides a stable state because this end-period P&L is the beginning P&L of the terminal value period. All period P&L must be normalised ie devoid of non-recurring or exceptional items. Normally the sales in the terminal period have an assumption of growth rate, which should be higher than the country’s inflation rate but lower than GDP growth rate. The sales growth rate in the explicit forecast period could be higher, if defensible. This is intuitive as the terminal period will run across periods of recession and so it cannot grow faster than the country’s GDP growth rate. It must be higher than the inflation rate otherwise the entity will not survive into perpetuity.

5. Weighted average cost of capital (WACC)

As all cashflows must be discounted to their present value as at date of valuation, an appropriate discount rate is required. The WACC is selected as a defensible rate for discounting as it is the weighted average of funding resources (equity and LT liabilities) and is the “hurdle rate” (minimum acceptable rate of return on invested capital) for assets and new investments. However, some income/revenue streams and cashflows are riskier due to political, country or industry and specific entity risks. The discount rate then must be adjusted upwards to address these additional risks.

It is important to note that the discount factor applied to cashflow streams is the factor 1/(1 + r)n where r is the discount rate and n is the number of years, and both are in the denominator of the factor. When r is bigger (higher risks), denominator is bigger and factor becomes smaller and this reduces the present values of the cashflows, which is intuitively correct. Likewise, when n is higher as the cashflows are more distant.

It is interesting to note that the cumulative present values of the 5-year explicit forecast period are much less than the PV of the terminal value. Although the terminal period is from the 6th year to perpetuity, the PV of each year gets smaller and smaller until it becomes miniscule after say, 50 or 80 years, depending on the size of the discount factor. And beyond that period, there is no significant increase in terminal value!

The discount factor 1/(1 + r)n over the period, cumulatively gravitates towards 1/r% for a regular cashflow stream to perpetuity and the factor is called the perpetuity factor. It has significant implications to computation of the terminal value and the application of the Gordon Model.

6. Gordon model for computation of Terminal Value and Enterprise Value (EV)

The Gordon Model formula is expressed as SCF X (1 + g)/(r – g) X 1/(1+ r)n

There are 3 factors in this formula.

a) SCF (Standard Cashflow) – This is the cashflow derived from a normalised 5th year P&L.

b) (1 + g)/(r – g) – this original perpetuity factor (1/r%) brings the constant stream of cashflows from the 6th to perpetuity to the beginning of the 6th year. But since there is a growth rate of g%, the numerator of the perpetual factor will have to increase by g% (ie 1 + g) to magnify individual forward cashflows, while the denominator must decrease by g% (ie r – g) to reduce or minimise the denominator thereby increasing the reciprocal of 1/(r – g) to indicate the growth.

You will notice that g cannot be equal or greater than r; otherwise the factor collapses!

c) 1/(1 + r)n – The Terminal or Residual Value (TV) is computed in 2 stages.

Stage 1 discounts TV to 31 Dec 2019 at $190,172. Stage 2 further discounts $190,172 to date of valuation at 31 Dec 2014. The discount factor applied is 1/(1 + 9%)5 or 0.650.

The diagram below depicts the computation of EV. The 5-year explicit forecast period covers years 2015 to 2019. The terminal value period starts from year 2020 to perpetuity. The FCF numbers are illustrative only.

Note that the discounted terminal value is about 4X the total discounted value of the 5-year explicit forecast period. It could be higher depending on the size of cashflow stream to perpetuity and the discount rate applied. This could be a good check on whether the EV is reasonable.

Note: FCF is lower in 2018 due to additional investment in committed CAPEX.

7. Adjusting from operating profit (EBIT) to cashflows

An illustration of the computation of FCF (Free Cashflow after tax) is as shown. As we are first computing EV (Enterprise Value), which belongs to the shareholders (Equity) and the bankers (Debt), we must start with EBIT (in which both shareholders and bankers have a share). EBIT is arrived after depreciation is deducted in expenses. Tax is then levied on EBIT for 2 reasons.

i) Discounted cashflow is an after-tax cashflow. Tax is an expense which must be settled.

ii) EBIT is after depreciation and so tax benefit on depreciation is granted upfront.

The resulting figure is EBIT after tax. But rather than calling it EBITAT (which confuses with EBITDA), I believe NOPAT is a better term to use since NOP (Net Operating Profit) is EBIT.

Depreciation (a non-cash item) is then added back to NOPAT to arrive at Cashflow after tax.

As increases in sales over the forecast period require additional working capital and CAPEX to support, such investments are deducted from Cashflow after tax to arrive at Free Cashflow (FCF). The stream of FCFs to perpetuity is then discounted using an adjusted (for risks, if required) WACC to arrive at EV.

Illustration

EBIT (earnings before interest & tax) , say 2,500

Tax at 17% (425)

NOPAT (net operating profit after tax) 2.075

Add back depreciation, say 600

Cashflow after tax 2,675

Less additional investments

Additional working capital, say (250)

CAPEX, say (400)

Free cashflow after tax 2.025

8. The Multiple-based Approach as a countercheck

To countercheck on the range of values obtained from the income method, we normally use the Multiple-based Approach or the comparative company approach, based on either

a) recent comparable acquisitions, or

b) comparable listed companies.

We shall then establish a multiple with numerator as the EV of the comparable company and the denominator, a suitable aggregate.

The aggregate could be

a) Revenue

b) EBIT

c) EBITDA or

d) Earnings

EV/EBITDA is normally preferred as a multiple for countercheck because of the following reasons.

a) Cashflows to perpetuity are discounted to present value in the income approach. So, using EBITDA (also Cashflow) as an aggregate is most appropriate.

b) Capital structures differ among companies, and it could distort comparison. EDITDA removes the impact of capital structure on P&L by excluding interest.

c) Likewise, tax expense could be different for various companies under different tax regimes. This “distortion” is also removed from EBITDA.

After the comparative range is computed, it must reconcile with the range obtained by the income method. One of the reasons for the differences in range values could be the additional investments (working capital & CAPEX) needed in arriving at the range of values under the income approach. Another reason could be the adjusted discount factor applied under the income approach.

9. Key steps in arriving at a range of values for business valuation

Step 1: Strategic Analysis of the company

In any valuation assignment, we must understand and learn more about the client’s company, business, and industry it operates in. More importantly, the drivers of the business, the stages of its major product life cycles, operationally cash generative or cash depletive, budgets, past financial history, corporate strategic plan, and business plan. This first step is critical because it helps the valuer to maximise the value of the company defensibly.

Step 2: Review/Establish the Business Plan

The corporate strategic plan and the business plan are crucial in establishing the forecast financial projections. The use of extended budget from 3 years to 5 years may not be adequate to maximise the value of the company because budgets are short-term exercises. In any case, for smaller assignments use of extended budget figures may be acceptable.

Step 3: Calculate a discount rate

Normally the discount rate is the WACC because it is the “hurdle rate” and is derived from capital structure. However, it must be adjusted for foreseeable risks in the business going forward, be it country-specific and/or entity- specific.

Step 4: Calculate discounted Terminal Value

The computation of TV is discussed in section 6 above.

Step 5: Compute Enterprise Value (EV) and Equity Value (EqV)

The computation of EV is also discussed in section 6 above. Normally Equity Value (EqV) is the required figure to start negotiation between the parties (potential buyer and seller). EV must be adjusted to arrive at EqV, as follows:

EqV = EV + non-operating assets + unrecorded assets (both tangible and intangible) less LT debt (net of cash balances) and unrecorded liabilities, if any.

It is to be noted that both EV and EqV are individual range of values, not single point values.

Step 6: Perform sensitivity analysis and review value range

Sensitivity analysis is best done using financial modelling whereby the output variables are EV and EqV and the input variables that drive the output variables are sales growth (for the 5-year explicit forecast period), terminal sales growth (g%), gross profit margin, and the discount rate (r%).

The range of values derived from sensitivity analysis is then counterchecked using another valuation approach.

Step 7: Countercheck range of values derived from income approach

The multiple-based approach is normally preferred for counterchecking. The process is discussed in section 8 above. When the differences between the 2 ranges of value are reconciled and explained, the business valuation of the EqV of the company is finalised.

10. Conclusion

It must be recognised that as Business Valuation is more an art than a science, no two valuations based on the same approach can produce the same outcomes. But the 2 ranges of values can be reconciled based on assumptions applied, the risk assessment of the valuation, the availability of the information provided by client or extracted from public sources, the defensibility of the figures, and how each valuer exercises his/her judgement and effort in maximising the range of value defensibly for the client.

References:

1. Nanyang Technology University, Introductory Business Valuation, CVA Programme, Level 1, Module 1. 2nd Edition, McGraw-Hill. 2019.

2. Business Valuation for Transactions, CVA Programme, Level 2, Module 3. McGraw-Hill 2019.

3. Tim Koller, et al. Valuation – Measuring and Managing the Value of Companies. 6th Edition, McKinsey & Company. 2015

4. Prasanna Chandra. Corporate Valuation and Value Creation. McGraw Hill. 2011

Note:

The opinions expressed, overtly or covertly, in this article are the author’s own and do not represent any pronouncements or opinions of any professional organisations or educational institutions.

———————————————End————————————————

NOTE to readers of this article:

For those who are new to business valuation (BV), studying a course in BV, or non-finance trained, you may wish to enrol for the following Masterclasses (Zoom-based, and taught by author himself) to enhance your knowledge and skillsets in the accounting and finance areas.

1) The Finance Managers’ Masterclass (Run 27, at this writing)

2) The Finance Leaders’ Bootcamp (Run 10, at this writing)

3) From Finance Leader to Strategic Thinker (Run 2, at this writing)

The Masterclass contents are available at www.cfodesk.com.sg .

You can also email me at mtclee@singnet.com.sg or mmleetc789@gmail.com for any further clarifications.

————————————————————————————————————-

Michael Matthew Lee’s credentials are:

Chartered Accountant (ISCA)

Chartered Marketer (CIM(UK))

MBA (Finance, NUS Business School)

MBA (Strategic Marketing, University of Hull)

BAcc (NUS); DipM (UK); PDipM (APAC); ACTA; PMC, CertEd

ASEAN CPA; FCA(Singapore); FCPA(Aust); FCCA(UK); FCIM(UK); MSID.

Note:

Michael has written 12 accounting & finance articles and they can be accessed through

Website: www.cfodesk.com.sg;

LinkedIn: “Michael M Lee”; and

Facebook: “Michael M Lee”

1) 8 Oct 2018: “Debit & Credit” – Upon this Rock, the House of Accountancy was built!

2) 17 Oct 2018: Financial Statement Analysis (an overview) – moving from lagging (historical) indicators to leading (predictive) indicators.

3) 26 Nov 2018: Traditional Financial Statement Analysis – using lagging indicators (Part 1)

4) 17 Dec 2018: Financial Statement Analysis – using leading indicators (Part 2)

5) 24 Jan 2019: Financial Statement Analysis – Is there an optimal capital structure? (Part 3)

6) 24 Feb 19: Financial Statement Analysis – What is V.I.S.A.? (Part 4)

7) 7 Apr 19: Financial Statement Analysis – The V.I.S.A. Approach (Part 5)

8) 26 Apr 19: Cashflow Statement – an enhanced presentation

9) 28 Jun 20: Cashflow Statement – Period & Trend Analysis

10) 3 Feb 21: The Economic Resources Approach to Accounting (ERAA)

11) 18 Apr 22: Business Valuation – A primer

12) 7 May 22: Business Valuation – Income Approach

Currently, embarking on writing a 2nd book entitled “Cashflow Sustainability and Corporate Growth” to be launched mid-2023, and is targeted for C-suite executives, locally and internationally. This book is a sequel to “The Essence of Corporate Cashflow Sustainability”.

————————————MMLee 7May22——————————–