Business Valuation – A primer

20 Apr, by

Biz Valuation – A primer

Business Valuation – A primer

1. Introduction

Business valuation is the process of determining the worth of an asset or a liability and it can be for an entire business, an ownership interest in the business or a specific asset or liability of the business.

Valuation is both a science and an art. As a science, it systematically applies well-defined theories and principles in deriving the value. But as an art, it requires subjective judgement based the objectives of the valuation, the facts and circumstances of the case, and the assumptions provided. As valuation is more art than science, there can be no precise value of the subject; it can only be found within a range of values.

2. The subject of valuation

It is important to clearly define the subject of valuation as the range of values could be different otherwise. As illustrative, a controlling stake in the ordinary shares in a company is much higher than a minority stake in the same company.

Other subjects of valuation could be

a) A business (a single company, a group of companies, selected companies in a group, etc)

b) Other types of equities such as preference shares, employee share option, etc

c) Corporate debts such as bank loans, bond, convertible bond, etc

d) Specific assets or intangible assets in a company such as derivative contracts, brands, patents, leasing agreements.

3. The reasons for valuation

The most common reason is in mergers and acquisitions (M&A) projects. There may be an opportunity to sell an existing business (divestment), buy a new business (acquisition) or merge existing business(es) with other business(es) (merger).

Other reasons are:

a) Transitioning a family business to other family members or other partners.

b) Seeking new funds to expand existing business

c) Taking in new partner(s) and the need to determine buy-in price

d) Retirement exit strategy involving pricing of business

e) Business partners/shareholders want to exit the business and valuation is required for business to be divided or dissolved.

f) Valuation requirement arising from financial litigation

g) Need to drive business value as company grows and expands.

h) Corporate restructuring

i) Taxation issues

j) Financial reporting requirements

4. How is valuation done?

There are certain steps a valuer must follow to ensure that the valuation engagement is proceeded along the right track.

Step 1.Define the engagement and the scope of work.

The valuer will need to know the subject of the valuation, the date of valuation, the conflict-of-interest areas, the type of report required, and the timing of the report.

Step 2. Obtain a clear understanding of the subject and the business.

Client engagement to find out more about the subject matter, the business and the industry is critical. Additional research from public sources is necessary to confirm and expand on knowledge acquired from client.

Step 3. Assess the availability and quality/reliability of information resources.

The reliability, credibility and defensibility of the valuation depend very much on the availability and quality of information obtained from the client and other relevant sources.

Step 4. Determine the appropriate valuation approach and methodology.

There are basically 3 valuation approaches and methodologies to select from. Depending on the objectives, facts ,and circumstances of the valuation an appropriate approach is selected. There is a need to explain in the final report why other approaches are not suitable.

Step 5. Determine the relevant valuation parameters and results.

The parameters are the factors that are necessary inputs for the valuation exercise. In the income approach using the discounted cashflow (DCF) method, the key parameters are the projected stream of cashflows (normally categorised into a 5-year explicit forecast and a terminal/residual value), the discount rate (which is the weighted average cost of capital), and the growth rate of the company.

The results obtained from the key inputs and assumptions based on business plan are a range of values.

Step 6. Perform sensitivity analysis (using financial modelling) and valuation cross-checks.

As business valuation is not a point concept because of its subjectivity based on relevant and defensible assumptions, valuer’s experience and judgements, a range of values is computed. This is normally performed using financial modelling on changes in key assumptions on a combination of projected sales, gross margins, growth rates, adjusted discount rates.

Cross-check on the range of values arrived at using the income approach is necessary to defend the values. Another approach such as market approach could be used for such cross-checks. The differences in values must be reconciled and explained.

5. Valuation approaches.

Basically, there are 3 valuation approaches commonly used. They are :

a) Market approach

It is a multiples-based approach whereby the value of the enterprise is determined by referring to the known value of other comparable enterprises either in recent M&A transactions or market capitalisation of comparable listed companies.

b) Income approach

This approach discounts a detailed future stream of cashflows for the enterprise at an appropriate discount rate. By far this income approach is most robust and comprehensible.

The stream of cashflows is derived from

i) a 5-year (normally) projected P&L based on assumptions supported by the company’s business plan, and

ii) a terminal value based on the 5th year normalised P&L, with a growth rate into the future

and adjusted for non-cash and non-operating items to arrive at EBITDA and then applying corporate tax rate on it to arrive at NOPAT (net operating profit after tax). At this stage it is cashflow after tax but not free cashflow after tax. Investments in additional working capital (to support growth in sales) and projected CAPEX are deducted to arrive at Free Cashflow after tax (FCF). The discount rate is then applied to FCF to arrive at Enterprise Value (EV).

The procedures in arriving at EV is more complicated than what is described briefly above as the computation of the discounted value of the terminal value is challenging and the valuer’s experience and good judgement play a big role in defensibly maximising the valuation range.

c) Asset-based approach

The aim is to value the assets and liabilities of the enterprise at their current fair market value and thus, determine an adjusted Net Asset Value (NAV).To arrive at Enterprise Value, there is then an additional calculation of goodwill to value the entire enterprise and not simply its NAV.

6. Who are the clients of the valuation assignment?

They are mainly:

a) Investors

b) Owners, company Board of Directors & management

c) Acquirers & vendors

d) Regulatory bodies

e) Accounting community

f) Legal community

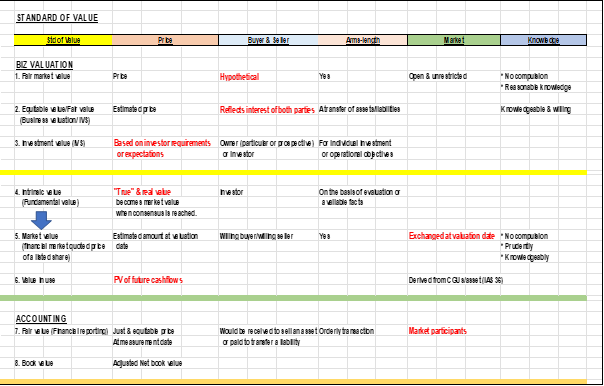

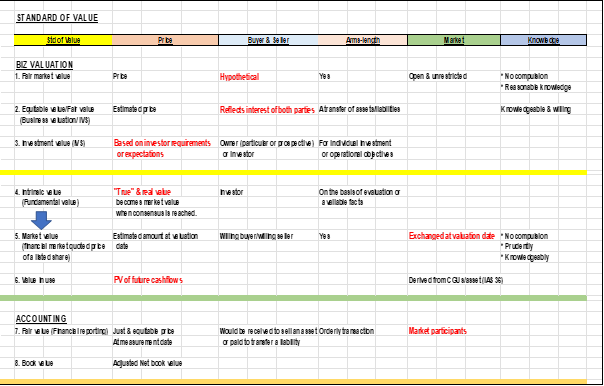

7. Premise and Standard of value.

These are 2 critical concepts that a valuer must be fully cognizant of. The first is the premise of value, which is the assumption regarding the most likely set of transactional circumstances that may be applicable to the subject. Basically, we need to know the status of the business, and the set of circumstances which could be actual or hypothetical. Two common premises of value are going concern or liquidation (orderly or forced). A clear knowledge of the premise of value allows us to select an appropriate standard of value, which is the second critical concept in valuation.

An actual set of circumstances requires an actual market transaction at arms- length and each party to the transaction performs their own valuation analysis leading to negotiation between the parties. Sometimes actual market transactions are not available as the business interest is not exposed for sale yet. In which case, a hypothetical or notional market valuation is required. This valuation is deemed to be assessed “theoretically” without an arms- length negotiation process. This concept is well-defined in valuation theory and standards (such as “fair market value”) and in financial reporting standards (such as “fair value”).

For an appropriate standard of value to be selected, we need to know

a) value to whom? and

b) under what facts and circumstances (including constraints, if any)?

The common standards of value are:

a) Fair market value

The price at which property would change hands

i) between a hypothetical willing and able buyer and a hypothetical willing and able seller,

ii) acting at arms-length,

iii) in an open and unrestricted market, when neither is under any compulsion to buy or sell, and when both have reasonable knowledge of the relevant facts.

b) Equitable value/Fair value (Business Valuation)

It is an estimated price for the transfer of an asset or liability between knowledgeable and willing parties that reflects the interest of those parties (IVS)

c) Fair value (Financial Reporting)

It is concept of adequate compensation (indemnity) consistent with justice and equity.

In accounting standards, fair value is the price that

i) would be received to sell an asset or

ii) paid to transfer a liability

iii) in an orderly transaction

iv) between market participants

v) at the measurement date (IRS)

d) Intrinsic value (Fundamental value)

The value that an investor considers, based on an evaluation or available facts, to be the “true” or “real” value (that is, the fundamental value) that will become the market value when the other investors reach the same conclusion.

e) Investment value

The value of a particular investor based on the individual investment requirements and expectations.

The value of an asset to a particular owner or prospective owner for individual investment or operational objectives (IVS)

f) Book value

The difference between total assets (net of depreciation, depletion, or amortisation) and total liabilities as they appear on the Balance Sheet (same as Shareholders’ Equity)

g) Value in use

The present value of future cashflows expected to be derived from an asset or cash generating unit (CGU) of a company is its value in use. The CGU is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cashflows from other assets (IAS 36)

h) Market value

The estimated amount for which an asset or liability

i) should exchange on valuation date

ii) between a willing buyer and a willing seller

iii) in an arms-length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion (IVS).

For a listed company, the quoted price of its listed share (ie its current market value) multiplied by the total number of shares on issue is its market value (financial market definition). As market price fluctuates moment by moment due to demand and supply factors, economic and political factors, besides its intrinsic value, the valuation date becomes critical.

i) Liquidation value

It is the amount that would be realised when an asset or group of assets are sold on a piecemeal basis. It also considers the costs of getting the assets into saleable condition as well as those of the disposal activity.

Liquidation value can be determined under

i) an orderly transaction with a typical marketing period, or

ii) a forced transaction with a shortened marketing period (IVS).

8. Standard of value and valuation purposes.

The table below shows a summary of appropriate standard of value that can be applied for each of the different valuation purposes.

It is noted that fair market value and market value are mostly applied standards of value. Fair market value is a hypothetical measure of the same facts and circumstances in the transaction that a willing buyer and willing seller are prepared to engage in. Market value is derived from the fundamental or intrinsic value of the subject, when with consensus in the marketplace gravitates towards market value.

9. Conclusion

Business Valuation is a relatively new profession and is an area where certain accounting standards and principles may not readily apply. As it is more art than science, it is incumbent on the valuer to apply his/her expertise, experience, knowledge, and competence to determine, defend and maximise the value of subject matter assigned.

References:

1. Nanyang Technology University, Introductory Business Valuation, CVA Programme, Level 1, Module 1. 2nd Edition, McGraw-Hill. 2019.

2. Tim Koller, et al. Valuation – Measuring and Managing the Value of Companies. 6th Edition, McKinsey & Company. 2015

3. Prasanna Chandra. Corporate Valuation and Value Creation. McGraw Hill. 2011

Note:

The opinions expressed, overtly or covertly, in this article are the author’s own and do not represent any pronouncements or opinions of any professional organisations or educational institutions.

NOTE to readers of this article:

Those who are new to business valuation (BV), studying a course in BV, or any non-finance trained, you may wish to enrol for the following Masterclasses (Zoom-based) to enhance your knowledge and skillsets in the accounting and finance areas.

- The Finance Managers’ Masterclass (Run 27, at this writing)

- The Finance Leaders’ Bootcamp (Run 10, at this writing)

- From finance Leader to Strategic Thinker (Run 2, at this writing)

The Masterclass contents are available at www.cfodesk.com.sg .

You can also email me at mtclee@singnet.com.sg or mmleetc789@gmail.com for any further clarifications.

Author’s Profile

Michael Matthew Lee is a trained teacher, lecturer, coach, and facilitator, and is himself a life-long learner.

Being trained, he is skilful in explaining difficult concepts in a simple and understandable manner. With his more than 40 years of corporate working experience, which include serving as Group CFO of 3 large Main Board public-listed groups, and as CXO (MD/CEO/COO) of various companies across industries, he specialises in Finance and Strategic Marketing and is exposed to senior executive management practices, issues, and challenges. He adopts a practical approach to his training and facilitation and draws case studies from actual cases (adapted) he personally managed over his 4 decades of corporate working experience.

Michael Matthew Lee’s credentials are:

Chartered Accountant (ISCA)

Chartered Marketer (CIM(UK))

MBA (Finance, NUS Business School)

MBA (Strategic Marketing, University of Hull)

BAcc (NUS); DipM (UK); PDipM (APAC); ACTA; PMC, CertEd

ASEAN CPA; FCA(Singapore); FCPA(Aust); FCCA(UK); FCIM(UK); MSID.

Note:

Michael has written 11 accounting & finance articles and they can be accessed through

Website: www.cfodesk.com.sg;

LinkedIn: “Michael M Lee”; and

Facebook: “Michael M Lee”

1) 8 Oct 2018: “Debit & Credit” – Upon this Rock, the House of Accountancy was built!

2) 17 Oct 2018: Financial Statement Analysis (an overview) – moving from lagging (historical) indicators to leading (predictive) indicators.

3) 26 Nov 2018: Traditional Financial Statement Analysis – using lagging indicators (Part 1)

4) 17 Dec 2018: Financial Statement Analysis – using leading indicators (Part 2)

5) 24 Jan 2019: Financial Statement Analysis – Is there an optimal capital structure? (Part 3)

6) 24 Feb 19: Financial Statement Analysis – What is V.I.S.A.? (Part 4)

7) 7 Apr 19: Financial Statement Analysis – The V.I.S.A. Approach (Part 5)

8) 26 Apr 19: Cashflow Statement – an enhanced presentation

9) 28 Jun 20: Cashflow Statement – Period & Trend Analysis

10) 3 Feb 21: The Economic Resources Approach to Accounting (ERAA)

11) 18 Apr 22: Business Valuation – A primer

Currently, embarking on writing a 2nd book entitled “Cashflow Sustainability and Corporate Growth” to be launched mid-2023, and is targeted for C-suite executives, locally and internationally. This book is a sequel to “The Essence of Corporate Cashflow Sustainability”.

————————————MML 18Apr22————————————