Cashflow Statement – Period & Trend Analysis

29 Jun, by

Cashflow Statement – Period & Trend Analysis

(To determine corporate cashflow sustainability)

By Michael M Lee

- Introduction

This paper is a follow-on discussion of my earlier paper entitled “Cashflow Statement (CFS) – An enhanced presentation “. It covers the most important and serious concern of the sustainability of a company’s cashflow position, using both Period and Trend CFS analyses to “uncover the truth”.

1.1 Why sustainability of cashflow is important?

The cashflow statement reconciles the cashflows between two points in time, normally between beginning and end of period/year. These cashflows are widely classified as operating, investing, and financing activities. Cashflow from operating activities is the most important because it funds the investment activities and draws resources from financing activities, if needed. It is the “heartbeat” of the company and must be positive and growing, to validate the company’s going concern assumption. If operating cashflows weaken, the company’s business may spiral downwards, and its survival is threatened.

The question then is how we determine if the company’s operating cashflow is sustainable, going forward.

1.2 Examining the current Cashflow Statement (CFS) presentation

As discussed in my earlier paper, the current CFS presentation allows choices in the treatment of interest expenses and interest income, among other items. The reason is that there is no clear guideline in defining “Cashflows from operating activities”. The CFS could begin with Profit after tax (PAT) or Profit before tax (PBT).

From the commercial or business point of view, business leaders would like to know what the cash component in PAT is, knowing full well that PAT includes non-cash items and delayed cashflows from working capital items. They also need to clearly see PAT from the Profit & Loss Statement continuing into the CFS to arrive at Cash PAT. So, the starting point in the CFS must be PAT and not PBT.

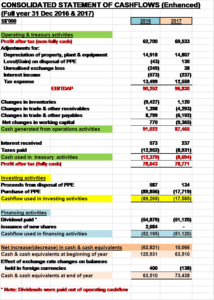

The proposed enhanced presentation of the CFS (in my earlier paper) is as depicted in the diagram that follows.

2. Period Cashflow Statement

2.1 Traditional analysis

For a first indication of sustainability, the Cashflow from operating (and treasury) activities must be positive and growing over the 2 comparative years. When it is positive, we will then analyse what investment activities it funds and whether it could also fund financing activities (repayment of loans, granting of dividends, etc) or investment activities have to be funded by financing activities. This appears to be the traditional analysis of the CFS.

Proposed enhanced presentation of CFS, highlighting “Cash PAT”.

2.2 Proposed analysis

On the use of cashflow from operating (and treasury) activities, the questions to ask are whether it is investing to

a) maintain the operating assets of the company, typically Plant & Equipment. This means whether the company is taking care of its motor vehicles and equipment to enable it to continue servicing sales (a going concern consideration), and/or

b) grow its operating assets (purchase or build a new building, more vehicles, more factory lines, etc) to enable the company to move to its next stage of growth (another going concern consideration). This investment must be in line with corporate strategy and plan. And that is why accountants and Finance Leaders are required to be strategic thinkers as well to participate in the company’s strategic and corporate planning.

In the diagram below, you can clearly see that the cashflow involvement in investing activities is actually addressing the right-hand side of the Balance Sheet, the operating resources side.

After investing activities, are the financing activities. Here, the questions to ask are:

a) are there enough cashflow left after investing activities to cater for financing activities, if not then

b) how is the company going to fund the cashflow inadequacy; by way of new bank loans or issue of new shares, rights issue, etc or utilising its brought-forward cash balances. This latter move could deplete cash balances (another going concern consideration).

Financing activities address the left-hand side of the balance Sheet, the funding resources.

Investing and financing cashflow activities could increase or grow total assets. Over a historical 3 to 5-year period, there must be growth in total assets to indicate corporate growth. Any reduction in total assets over the period signals a depletion of total assets, which could threaten going concern assumption. However, this does not indicate whether cashflow is sustainable, which requires Trend CSF Analysis to enlighten and determine.

3. Trend Cashflow Statement

The Trend CFS Analysis requires at least 4 years of past CFS, for effect. This would provide 3 years of trend in PAT and Cash PAT, the twin engines for cashflow sustainability tests. In normal situations, Cash PAT must be greater than PAT as the latter is arrived at after deducting depreciation, amortisation and provisions. The gap between Cash PAT and PAT must therefore be positive.

The diagram below shows the trends of PAT, Cash PAT and Cash PAT Gap movements over a 4-year period.

a. Situation 1:

When PAT is uptrend and Cash PAT is downtrend (divergent), future PAT is likely to decrease because there will be insufficient cash resources to fund operations adequately in the future.

b. Situation 2:

When PAT is downtrend and Cash PAT is uptrend (convergent), there may be overprovisions in P&L and/or cash is not utilised for operations growth. This situation is unsustainable.

c. Situation 3:

When PAT is uptrend and Cash PAT is also uptrend (in line), there is stability in cashflow and this situation is what we are looking for over a period of time – there is sustainability of cashflow.

Over the period the cashflows may not trend neatly and that is no cause for alarm as it can be tweaked or fixed in the next season.

4. Conclusion

Both Period and Trend Cashflow Statements must be analysed to determine whether the company is achieving cashflow sustainability. By purely reviewing the P&L Statement for growth in profits and then analysing CFS for the trend in Cash PAT may not be the end all. There is still a missing link, which is the growth of the operating resources (total assets) in the Balance Sheet and the refunding of the funding resources (equity & LT liabilities). At the macro level, cashflow sustainability must also be supported by growth in operating resources.

——————————-MMLee 28June2020——————————

Note: The new ideas, principles, and concepts presented in this paper are the author’s own and do not represent those of any institution or organisation.

About Michael Matthew Lee

Michael M Lee is a trained teacher, lecturer, coach and facilitator, and is himself a life-long learner. He is currently pursuing the Chartered Valuer & Appraiser Programme at Nanyang Business School.

Being trained, he is skilful in explaining difficult concepts in a simple and understandable manner. With his more than 40 years of corporate working experience, which include serving as Group CFO of 3 large Main Board public-listed groups, and as MD/CEO/COO of various companies across industries, he specialises in Finance and is exposed to senior executive management practices, issues and challenges. He adopts a practical approach to his training and facilitation.

Michael also runs his own company, The CFO Desk Pte Ltd, which is engaged in financial consultancy (corporate restructuring, IPO advisory, cashflow management) and business valuation, besides corporate training and public seminars.

Michael M Lee’s credentials are:

MBA (Finance, NUS Business School)

MBA (Strategic Marketing, University of Hull)

BAcc (NUS); DipM (UK);; PDipM (APAC); ACTA; PMC

ASEAN CPA; FCA(Singapore); FCPA(Aust); FCCA(UK); FCIM(UK); MSID.

Note:

Michael has already written 8 accounting & finance articles to-date and they can be accessed through

Website: www.cfodesk.com.sg;

LinkedIn: “Michael M Lee”; and

Facebook: “Michael M Lee”

- 8 Oct 2018: “Debit & Credit” – Upon this Rock, the House of Accountancy was built!

- 17 Oct 2018: Financial Statement Analysis (an overview) – moving from lagging (historical) indicators to leading (predictive) indicators.

- 26 Nov 2018: Traditional Financial Statement Analysis –using lagging indicators (Part 1)

- 17 Dec 2018: Financial Statement Analysis – using leading indicators (Part 2)

- 24 Jan 2019: Financial Statement Analysis –Is there an optimal capital structure? (Part 3)

- 24 Feb 19: Financial Statement Analysis – What is V.I.S.A.? (Part 4)

- 7 Apr 19: Financial Statement Analysis – The V.I.S.A. Approach (Part 5)

- 26 Apr 20: Cashflow Statement – an enhanced presentation