Financial Statement Analysis – Is there an optimal capital structure? (Part 3)

31 Jan, by

Author: Michael M Lee

- Introduction

This is the 3rd accounting & finance article of my 5-Part Financial Statement Analysis (FSA) series. In this article I shall discuss capital structure; its importance and implications to financial management and operational success. Much of the discussion will be centred on the practical aspects rather than its theoretical underpinnings (ie setting aside Modigliani & Miller Theorem and Robert Hamada’s Equation).

- What is capital structure?

In my article “Financial Statement Analysis- using lagging indicators (Part 1)” I talked about the economic resources approach to accounting (ERAA) in which “funding resources” (right hand side of Balance Sheet) is the starting point in any enterprise or business. The funding resources comprise equity (shareholders’ capital and revenue reserves) and long-term liabilities (LTL). The proportion between equity (“internal” capital) and LTL (“external” capital) is called capital structure.

Both equity and LTL have their own costs. LTL, which is basically funding from banks levy interest at known/negotiated rates. The cost of equity is more difficult to assess, but it is certainly much higher than cost of LTL. This is because equity shareholders get nothing when the company that they invested in goes under. They are not protected by security or covenants, which the banks demand. Technically, the cost of equity is calculated based on the “capital asset pricing model” or CAPM.

The combined cost of equity and LTL is based on the CAPM cost (cost of equity) and interest cost (cost of bank borrowings) weighted by the proportion of equity and LTL. In short, it is the “weighted average cost of capital “ or WACC

The technicalities of WACC and CAPM and the critical issue of how the company is going to satisfy the shareholders’ cost of equity will be explained in my future accounting articles.

For now, we just understand that the average cost of funding resources (left hand side of Balance Sheet) is WACC.

- Why is capital structure important?

Capital structure is important for 2 reasons:

a) it addresses the adequacy of funding resources to support operating resources, which in turn enables operations to be executed without a hitch.

b) the proportion of equity to LTL (or leverage) will affect the quantum of interest expense that the company must shoulder. The higher the interest expense, the higher the financial risk.

- Leverage and risks

Before we discuss how capital structure affects the Profit & Loss Statement, we must understand leverage and risks.

4.1 Operating leverage and business risk

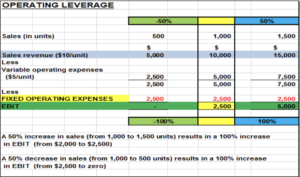

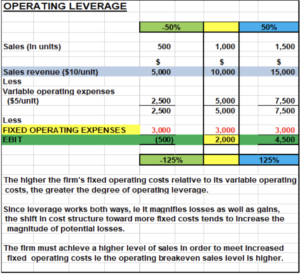

On the operations side, there are operating leverage and business risk. Operating leverage is achieved by leveraging sales on fixed operations costs (FOE) to magnify increases in EBIT (earnings before interest and tax). FOE is the lever and the longer the lever, the higher the leverage or magnification. Therefore, the greater the FOE, the more the leverage on EBIT. But sales increases must be able to cope with a higher increase in FOE.

The reverse is true. Negative leverage arises when there is a decrease in sales, which will magnify the decrease in EBIT via FOE.

Diagrammatically and arithmetically, operating leverage is represented as follows:

It can be seen from the arithmetic that the magnification is intuitive. As soon as FOE is covered by gross profit, the next dollar of gross profit goes straight to EBIT, thereby magnifying its increase immediately.

It can be seen from the arithmetic that the magnification is intuitive. As soon as FOE is covered by gross profit, the next dollar of gross profit goes straight to EBIT, thereby magnifying its increase immediately.

If growth in sales is slowing down, then there is a risk of sales not being able to capitalise on leverage. In which case, business risk sets in.

Business risk is the risk of sales not being able to cover both cost of sales and FOE adequately and management must be prepared to moderate the risk.

The 3 major components of FOE which normally add up to about 60% of FOE (depending on company and industry) are

a) salary costs

b) rental expenses

c) depreciation

To moderate the impact of weakening sales on business risk, management will have to cut back on the 3 major expenses. These actions will have to be planned, proactively rather than reactively.

4.2 Financial leverage and financial risk

On the finance side, there are financial leverage and financial risk. Financial leverage is achieved by leveraging EBT on interest expense to magnify increases in EPS (earnings per share). Interest expense is the lever and again, the longer the lever, the higher the leverage or magnification. Therefore, the greater the interest expense, the more the leverage on EPS. But EBIT increases must be able to cope with a higher increase in interest expense. Interest expense arises from LTL (typically bank borrowings), which defines capital structure.

The reverse is true. Negative leverage arises when there is a decrease in EBIT, which will magnify the decrease in EPS via interest expense.

Diagrammatically and arithmetically, financial leverage is represented as follows:

With the knowledge of the arithmetic, is it then easy to orchestrate a higher increase in EPS with a small increase in sales?

It depends on whether

a) sales is growing and sustainable, and

b) there is an exit plan for reducing FOE and interest costs when the economy turns south.

4.3 Leverage, risk and capital structure.

We have set aside the theoretical aspects of capital structure in this discussion as it can be very complicated and difficult to grasp. However, the theory allows us to view the capital structure issue from another perspective; it also helps “nourish the soul”.

From the practical viewpoint, I have designed the diagram below to summarise the concepts and the decision-making flow.

Depending on company and industry, there is always a set of fixed operating expenses (FOE) to run the business. We must know the breakeven sales to cover the FOE fully. Beyond that sales level, the operating leverage begins to kick in. What then is the level of sales that

-

- a) does not allow business risk to set in and

- b) allow a healthy operating leverage?

In practice, the measure of that level of sales is in the ratio EBIT/Sales. If the ratio is say 6% and the company’s competitors and peers are doing 7%, then business risk may just be on the horizon. But if the company’s EBIT/Sales at say, 8% or 10%, then operating leverage is sustainable. It is then time to consider an increase in interest expense to take more advantage of financial leverage.

The above diagram shows that a healthy operating leverage (after crossing the business risk threshold) is an input to capital structure management or how much additional L-T debt can the company work with.

Additional L-T debt will increase interest expense to the extent that it may pose a financial risk. The measure of financial risk is the interest coverage ratio or EBIT/interest. This ratio is compared against competitors’ and peers’. When the financial risk threshold is crossed, financial leverage is achieved.

- Why capital structure is important to FSA?

In the foregoing discussion, we learnt how capital structure can have a significant impact on P&L, PAT and EPS via interest expenses. When the metrics of business and financial risks ie EBIT/Sales and EBIT/interest respectively are not closely monitored, we lose sight of any potential threat to the “going concern” assumption of the company. FSA therefore must be cognizant of this cruel fact.

6. What are the practical constraints in increasing L-T debt?

Increasing debt in the capital structure may not come easy and there are the following constraints.

-

- Cashflow – ability to service debt is an important consideration

- Revenue stability – a more predictable and stable revenue stream is better for capital structure management

- Control (shareholders) – certain major shareholders may be adverse to borrowing too much, with good reasons

- Contractual obligation – which does not allow for further L-T borrowing

- Management preferences – highly risk averse?

- External risk assessment – economic and political environment in the short and longer term is a significant consideration

- Timing (interest rate environment) – in periods of high interest rates, borrowing is to be avoided.

7. Is there an optimal capital structure?

An optimal capital structure is achieved when with an appropriate mix of equity and debt, the WACC is at its lowest, and interest expenses (which impact P&L) are low too. In practice, it is difficult to achieve an optimal capital structure because L-T debt (and interest rates) is not determined or can be orchestrated by the company. It is determined by the banks!

The banks will only increase the company’s L-T debt when the company has a good forward story to tell, financial and operational performance is acceptable and most of all, it must have the projected cashflow to service principal and interest.

8. Conclusion

This article discusses one of the most important areas in Finance, the capital structure. The knowledge of capital structure management goes hand in hand with leverage and risks. FSA must cover this area of analysis, which is a leading indicator of any potential threats to “going concern” assumption of the company.

Note:

Michael M Lee’s other accounting articles in website: www.cfodesk.com.sg;

LinkedIn: “Michael M Lee”; and Facebook: “Michael Lee” are:

-

-

- 8 Oct 2018: “Debit & Credit” – Upon this Rock, the House of Accountancy was built!

- 17 Oct 2018: Financial Statement Analysis (an overview) – moving from lagging indicators to leading indicators.

- 26 Nov 2018: Traditional Financial Statement Analysis – using lagging indicators (Part 1)

- 17 Dec 2018: Financial Statement Analysis – using leading indicators (Part 2)

-

——————————-MMLee 24th Jan 2019—————————-