Financial Statement Analysis – What is V.I.S.A.? (Part 4)

31 Jan, by

Author: Michael M Lee

1. Introduction

In this penultimate part of my 5-part series on Financial Statement Analysis (moving from lagging to leading indicators), I shall discuss the areas in the financial statements (Balance Sheet, P&L Statement, and Cashflow Statement) in which accountants/CFOs and CEOs are seriously concerned about, agonising over the sustainability of the firm’s operational and financial performance. This is more so when the firm’s business or the economy heads south.

2. The economic resources approach to accounting (ERAA)

In my article “Financial Statement Analysis – using lagging indicators (Part 1)” I promulgated the economic resources approach to accounting (ERAA) in which “funding resources” is the starting point in any enterprise or business. The funding resources comprise equity (shareholders’ capital and revenue reserves) and long-term liabilities (LTL). The proportion between equity (“internal” capital) and LTL (“external” capital) is called the capital structure.

With an appropriate capital structure, operating resources are acquired for operations or expansion. The results of operations are then captured in a Profit & Loss Statement (P&L) which begins with sales and ends with PAT (Profit after tax). The P&L has 2 parts, viz. transactions or operations (from Sales to EBIT or operating profit), and treasury (interest and tax). Therefore, the KPI (key performance indicator) of the division head is based on EBIT and not on PAT as, most of the time, he has no control over treasury matters.

Intuitively, we know that PAT is not fully represented in cash because most of the sales are on credit (the firm is funding the customers) and some of the costs and expenses are also on credit. In cash terms (suppliers are funding the firm), there is no equal or timely matching of sales and costs/expenses. Cash collected from customers are not only used to pay for inventory and various suppliers, but also to pay bank loans, loan interests, purchase of fixed assets, pay dividends, etc.

The accountant therefore must account for the flow of cash from one point (beginning of financial year) to the next (end of financial year). A Cashflow Statement is then prepared to show how cash is generated and applied to and from operations, investments and financing, between the 2 points in time.

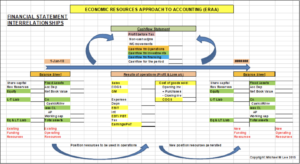

The ERAA diagram below depicts the financial statement inter-relationships and the logical accounting and transactional flows, as discussed.

We shall now look at the financial statements broadly and indicate what the accountant/CFOs and CEO should be concerned about ie what keeps them awake at night!

3. Left-hand side of Balance Sheet

Funding resources reside on the left-hand side of the Balance Sheet and these are the most critical resources in ensuring that the firm’s operations are executed without a hitch. If assets are not adequately funded, operations cannot continue. There will not be enough inventory to sell, not enough vehicles to transport the products to customers’ locations, etc. Therefore, we must always ensure ADEQUACY of funding resources!

Having determined that Adequacy of funding resources is key, the follow-up questions are:

a) How do we assess that funding resources are not adequate?

b) How much additional funding is needed to satisfy adequacy?

c) What capital structure is appropriate?

These questions will be discussed in Part 5 of my 5-part series.

4. Right-hand side of Balance Sheet

Fixed assets, investments, and current assets are on the right-hand side of the Balance Sheet. These are acquired by the funding resources. Through the passage of time, these operating resources may lose its original value or impaired. This may be due to inventory getting obsolete, accounts receivables not collecting on time or turning bad, cash in foreign currencies losing its value due to weakness in the foreign currency, and fixed assets requiring replacement. Therefore, we must ensure that assets or operating resources do not suffer from IMPAIRMENT.

The follow-up questions are:

a) How do we assess that certain classes of assets are impaired?

b) How do we prevent impairment from happening?

c) What level of total assets or operating resources are needed to minimise the occurrence of impairment?

These questions will be discussed in Part 5 of my 5-part series.

5. Profit & Loss (P&L) Statement

In the past, extraordinary items and exceptional items are part and parcel of the P&L Statement. These are no longer allowed as they tend to distort performance. A further improvement is the adoption of Other Comprehensive Income (OCI), which captures exchange/translation differences, revaluation gains/losses of property, etc. Some of these items were previously taken directly into revenue reserves and therefore transparency is in question. OCI is shown either as a separate statement from the P&L Statement or as part of P&L Statement.

VOLATILITY of operating results has always been an issue because it makes inter-period and intercompany comparisons challenging. Now that the big items that can cause volatility reside in OCI, the only volatility in P&L proper is sales performance, which can be monitored and explained.

Arising from volatility, the key questions to ask are:

a) How do we minimise volatility in P&L?

b) How do we monitor volatility?

These questions will be discussed in Part 5 of my 5-part series

6. Cashflow Statement

The cashflow statement is the most important financial statement as it shows the flow of cash within and without the firm, over two points in time. Out of the 3 activities (operating, investment and financing) the firm is involved in, cashflow from operating activities is vital to the firm’s financial health. It must be SUSTAINABLE!

The key questions to ask about sustainability are;

a) How is sustainability defined?

b) How can we ensure sustainability of operating cashflow?

These questions will be discussed in Part 5 of my 5-part series.

7. What then is V.I.S.A.?

It is now clear that V.I.S.A. is the acronym for

a) Volatility

b) Impairment

c) Sustainability, and

d) Adequacy.

The natural order of adequacy, impairment, volatility, and sustainability is important as depicted in the diagram below.

8. Conclusion

V.I.S.A. captures the concerns of accountants/CFOs and CEOs especially when the firm is not performing well operationally and financially. With financial statement analysis using both lagging and leading indicators in assessing V.I.S.A. and taking appropriate preventive/proactive and corrective/remedial actions, the accountant/CFOs and CEOs now have good tools to alleviate their concerns. Such a discussion will be presented in my final part of my 5-part series on financial statement analysis.

Note:

Michael M Lee’s other accounting articles in website: www.cfodesk.com.sg; LinkedIn: “Michael M Lee”; and Facebook: “Michael Lee” are:

- 8 Oct 2018: “Debit & Credit” – Upon this Rock, the House of Accountancy was built!

- 17 Oct 2018: Financial Statement Analysis (an overview) – moving from lagging indicators to leading indicators.

- 26 Nov 2018: Traditional Financial Statement Analysis – using lagging indicators (Part 1)

- 17 Dec 2018: Financial Statement Analysis – using leading indicators (Part 2)

- 24 Jan 2019: Financial Statement Analysis – Is there an optimal capital structure? (Part 3)

——————————-MMLee 24th Feb 2019—————————-