Stock options trading & investment – An introduction

05 Dec, by

1. Introduction

In Rich Dad advisor Andy Tanner’s book “Stock Market Cashflow” on page 220 “How Warren Buffet generates huge profits with options”, Andy wrote, “Buffet sells a lot of options. Why? Because he understands how time decay works to the benefit of the option seller. Options provide him with a great tool to generate additional income for his holding company.” Thus, options can be used to generate additional income. It can also be used for hedging and speculation.

To explain what Andy Tanner meant, let us consider the following illustration.

When a stock is bought say, at $2 and held for long term say 10 years. During that period, it may hit a high of $6 and roller coaster down to $2 at the end of 10 years or worse, to $1.Thus a stock held to long term may not be a winning proposition, unless yearly dividends are given to cushion any subsequent capital losses. There are basically 2 approaches to avoid this situation.

a) First, have a desired target return of say 20% and when it hits $2.40, the stock is sold. Then wait for it to move down to $2 again to reinvest and repeat the cycle. But this requires good tracking of the stock by applying technical analysis and knowing the recent historical “floor” and “ceiling” of the stock price.

b) The second approach is to sell a call option on the stock (a covered call) and collect “premium” regularly. This is akin to renting your house out regularly and collecting rental income.

2. What is a call option?

A call option is a financial contract that gives the holder the right, but not the obligation, to buy a stock at a certain price up to a certain date.

There are 4 elements in this definition.

- a) The right, but not the obligation (the right)

- b) Buy a stock (the underlying asset)

- c) At a certain price (the strike price)

- d) Up to a certain date (the expiration date)

Call options are used by traders who expect an increase in the price of the underlying asset.

3. What is a put option?

A put option is a financial contract that gives the holder the right, but not the obligation, to sell a stock at a certain price up to a certain date.

There are also 4 elements in this definition.

- The right, but not the obligation (the right)

- Sell a stock (the underlying asset)

- At a certain price (the strike price)

- Up to a certain date (the expiration date)

Put options are used by traders who expect a decrease in the price of the underlying asset.

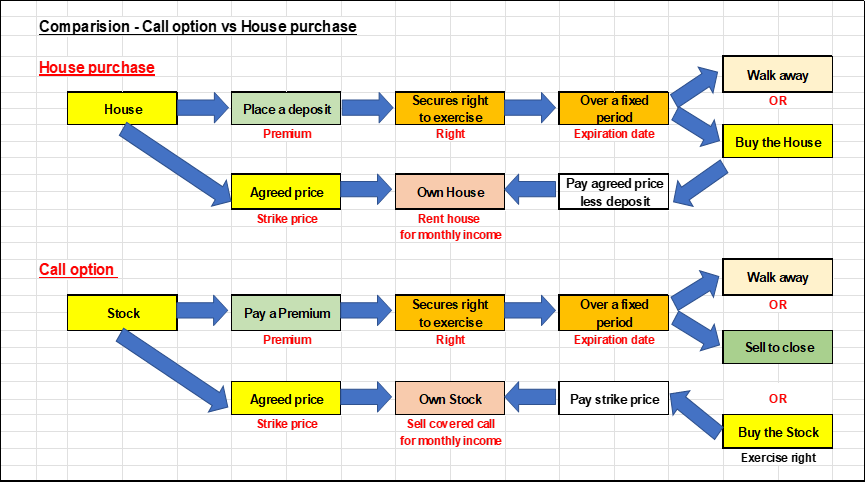

Figure 1: Call option vs House purchase

4. Comparison between call option and house purchase

Figure 1 shows a schematic diagram of the key processes separately, in a call option and in a house purchase. Both are purchases of an asset. A call option is a purchase of a stock. Both start off with the identification of the asset to be purchased and a deposit is placed as good faith money, allowing the purchaser a period to consider. In the call option this deposit is called premium, and the end of the period granted is the expiration date. The deposit entitles the purchaser to decide whether to

a) purchase the asset or

b) walk away, losing the deposit or premium in the process. In the stock purchase case, this arises when the stock price falls below the contracted price (strike price). In other words, the call option is “out of the money” and the call option is allowed to expire worthless.

If the purchaser decides to buy the asset, the house purchaser pays up the balance of the purchase price of the house. In the call option case, the buyer pays the strike price. Unlike the house purchaser, the deposit or premium is not deductible from the strike price. The premium is earned by the seller of the call option. The decision for the call option purchaser to exercise the option (buy the stock) arises from the fact that the stock price has increased vis-a-vis the strike price. In other words, the call option is “in the money”.

5. Why trade in options?

a) Income

- covered call, cash-secured sold put

When you sell (or write) a call option, you receive premium (an income) from the buyer of the call option. If the stock price rises, there is a chance that the buyer exercises the option and collect the stock from you. If you do not have the stock to cover your sell position (ie a ‘naked” position), you are exposed to pay a higher price to buy the stock from the market. But if you have the stock, you can just deliver the stock. In this case, you have made a covered call.

Covered calls are income generating trades when you know the fundamentals and technical characteristics of your stock.

You can also sell a put option and collect premium (income) from the buyer. In this case, you are giving the buyer the right to sell the stock to you at the strike price. When the stock price decreases below strike price, the buyer of the put will exercise his right and sell his stock to you, thereby making a gain for himself, net of premium paid. If you have stand-by cash to pay for the stock, you have done a cash-secured sold put option and since you have collected the premium upfront, the price of the stock purchased from the buyer of the put option is reduced.

b) Protection

- Protective put

When you buy a stock at $10 and it goes up to $20, but you still believe there is further upside, after studying the technical charts. To protect your profit against unexpected price declines, you can buy a put at strike price $15 for say, 3 months, by paying a premium (a fee). If the price does decline going forward, you can close the put option position.

c) Hedging

Options trading is a convenient and effective way to hedge against sudden price declines of the underlying stock as can be seen in a protective put exercise.

d) Speculation

Traders take a market betting position of a stock when they speculate. Instead of buying the stock directly which could be costly, they use options, which are cheaper and provides good leverage.

e) Diversification

Adding options trading strategies in a stock portfolio helps to cushion huge losses in a down-trending market. It therefore becomes part and parcel of a diversification of the stock portfolio.

f) Buy stock at a lower price

This the same as cash-secured sold put.

6. Characteristics of options

It is important to understand the features of options and how they collectively determine an option trade. These features are:

a) Underlying stock – an option is a derivative of the underlying stock

b) Standardisation – an option contract is normally traded at 100 shares of the underlying security.

c) Strike price – it is a fixed and determined price of the underlying stock to be traded. It is different from the market price, which is fluctuating, moment by moment if the stock is volatile.

d) Premium – a fee paid by the buyer of an option trade and is determined by Black Scholes model

e) Expiration date – it is the last day after which the option contract is no longer in effect.

f) Type – call, put (buy, sell) – An option contract must specify pertinent details, chief of which is the type of option to trade in.

7. Options vs Stocks

Briefly, options trading has more flexibility over stock trading. As options are derivatives, they can help to protect the underlying stocks from price declines.

a) Stocks

- Buy, sell, or hold

b) Options

- Calls: buy or sell

- Puts: buy or sell

They can be traded in Up markets, Down markets, and Sideways markets.

8. Basic Option Order

To place an option trade, the trader must follow certain standard rules, which require the trader to articulate each component of the trade in a specific order. The components of the option trade are:

A – Action (Buy to open/close; Sell to open/close)

C – Contract (Number of contracts)

U – Underlying stock

E – Expiration date

S – Strike price

T – Type (call or put)

P – Premium

To help us remember the presentation of the options order, we can use the mnemonic

ACU E SToP

(Acute Care Unit, Emergency, SToP)

9. ITM, ATM and OTM

These are

a) In the money (ITM)

b) At the money (ATM), and

c) Out of the money (OTM)

and they are characteristic of an option trade, which expresses the relationship between the market price of the stock and its strike price.

As illustrative, when you buy a call at $2 strike price and the current price is higher than $2, say $2.50, then the option is ITM (ie. A gain of $0.50 when exercised). When the current stock price is at $2, then the option is ATM (ie. No gain or loss when exercised). When the current stock price is below $2, say $1,80, the option is OTM (ie. A loss of $0.20 when exercised).

10. Conclusion

Options are useful instruments in protecting stocks from price declines. To apply them effectively, we must first understand the characteristics and mechanics of options trading and investments. As they are derivatives, the behaviour of the underlying stocks must be properly analysed and assessed. This would require knowledge of the technical charts and the fundamental analysis of the underlying stocks, without which options trading, supposedly applied as a protective measure, ends up as a speculative exercise!

‘——————————————–END——————————————

Disclaimer

Option trading & investment is risky and may not be suitable for everyone. It involves risk and you may lose money.

This article is written for education purposes only and not an invitation to engage in option trading and investment. Such decisions are very private and personal and requires a truthful examination of the mantra “Know Thy Self, Know Thy Plan, and Know thy stocks”.

‘———————————————————————————————————

Author’s Profile

Michael Matthew Lee is a trained teacher, lecturer, coach, and facilitator, and is himself a life-long learner.

Being trained, he is skilful in explaining difficult concepts in a simple and understandable manner. With his more than 40 years of corporate working experience, which include serving as Group CFO of 3 large Main Board public-listed groups, and as CXO (MD/CEO/COO) of various companies across industries, he specialises in Finance and Strategic Marketing and is exposed to senior executive management practices, issues, and challenges. He adopts a practical approach to his training and facilitation and draws case studies from actual cases (adapted) he personally managed over his 4 decades of corporate working experience.

He authored his first Finance book entitled “The Essence of Corporate cashflow Sustainability”, launched in June 2022.

Michael Matthew Lee’s credentials are:

Chartered Accountant (ISCA)

Chartered Marketer (CIM(UK))

MBA (Finance, NUS Business School)

MBA (Strategic Marketing, University of Hull)

BAcc (NUS); DipM (UK); PDipM (APAC); ACTA; PMC, CertEd

ASEAN CPA; FCA(Singapore); FCPA(Aust); FCCA(UK); FCIM(UK); MSID.

Note:

Michael has written 13 accounting & finance articles and they can be accessed through

Website: www.cfodesk.com.sg;

LinkedIn: “Michael M Lee”; and

Facebook: “Michael M Lee”

- 8 Oct 2018: “Debit & Credit” – Upon this Rock, the House of Accountancy was built!

- 17 Oct 2018: Financial Statement Analysis (an overview) – moving from lagging (historical) indicators to leading (predictive) indicators.

- 26 Nov 2018: Traditional Financial Statement Analysis – using lagging indicators (Part 1)

- 17 Dec 2018: Financial Statement Analysis – using leading indicators (Part 2)

- 24 Jan 2019: Financial Statement Analysis – Is there an optimal capital structure? (Part 3)

- 24 Feb 19: Financial Statement Analysis – What is V.I.S.A.? (Part 4)

- 7 Apr 19: Financial Statement Analysis – The V.I.S.A. Approach (Part 5)

- 26 Apr 19: Cashflow Statement – an enhanced presentation

- 28 Jun 20: Cashflow Statement – Period & Trend Analysis

- 3 Feb 21: The Economic Resources Approach to Accounting (ERAA)

- 18 Apr 22: Business Valuation – A primer

- 7 May 22: Business Valuation – Income Approach

- 24 Sept 22: Corporate Cashflow Sustainability – The foundation for corporate growth.

Currently, embarking on writing a 2nd book entitled “Cashflow Sustainability and Corporate Growth” to be launched mid-2023 tentatively, and is targeted for C-suite executives, locally and internationally. This book is a sequel to “The Essence of Corporate Cashflow Sustainability”.

————————————MML 4Dec22————————————