The Economic Resources Approach to Accounting (ERAA)

05 Feb, by

The Economic Resources Approach to Accounting (ERAA)

By Michael Matthew Lee

1. Introduction

Traditional accounting embraces the entity concept, which is good for explaining debits & credits, and what the entity owns and owes. But as businesses evolve, sustainability of cash and cashflows becomes vital, while the emphasis on entity and its going concern assumption remains important. Without cash and cashflows there is no entity, let alone going concern! Most companies painfully experience this situation during the current world-wide pandemic!

Cash is the most vital economic resource for an entity‘s survival and so my proposed new concept and approach is called “The Economic Resources Approach to Accounting” (ERAA), shifting the focus from Entity to Economic Resources. The financial statements must reflect Cash and Cashflows as the critical economic resources, and their inter-connectedness from Balance Sheet to Profit & Loss, to Cashflow Statement and back to Balance Sheet. This would enhance the businessman’s understanding of where the business is heading.

2. Business owner/Board/CEO’s demands for financial clarity

The current set of financial statements (Balance Sheet (B/S), Profit & Loss Statement (P&L) and Cashflow Statement (CFS)) does not directly enlighten business managers (collectively Business owner/Board/CEO) in the following queries/concerns.

- How are funding resources allocated?

- How are the allocated resources performing?

- How could re-allocation of resources be done?

- For the period, is operational performance shareholder value enhancing or shareholder value eroding? In which specific areas?

- What is the cash component in profit after tax (PAT) for the period?

- Where has the cash gap (P&L PAT vs Cash PAT) gone to?

- How is cash PAT applied? Is it appropriately applied to enhance corporate growth and shareholder value?

3. What are the drawbacks in the Entity Approach?

While we recognise that the Entity Concept is still the fundamental component of the Accounting Framework, it does not serve a useful purpose when it is applied to accounting presentation for business managers and investors.

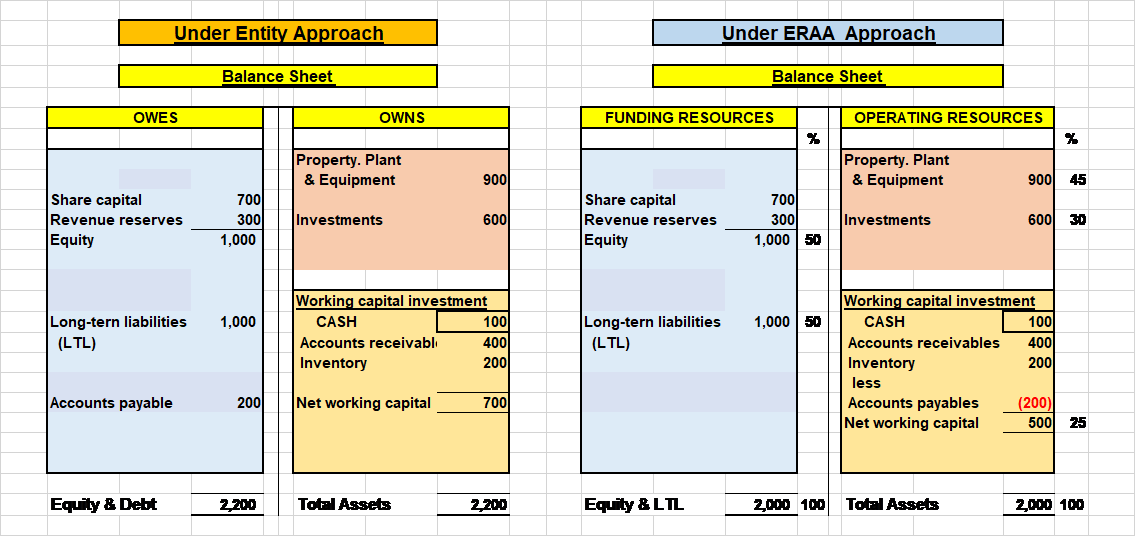

a. Accounts Payable (AP) is on the left-hand side (LHS) of B/S.

AP is on the LHS because it is what the entity owes to suppliers/creditors. But as an economic resource it is part and parcel of working capital investment and should be treated as such. We are so entrapped by the Entity Approach that we failed to recognise this economic and resource reality!

b. Impact of AP on financial ratios and total assets

Debt/equity ratio becomes distorted when AP is included in debt. When AP is high, cash and/or accounts receivable remain high, but these should be netted off against AP in net working capital, thereby having no impact on debt/equity ratio. Furthermore, total assets increase when AP is high and over the period it would appear that the company is in growth mode, when it is not.

c. Cash balances in working capital should only be operational cash.

Sometimes periodic idle cash distorts working capital needs. As a consequence, the additional working capital required to support sales growth is unnecessarily amplified. For better appreciation, only operational cash should be included in working capital.

Another problem with leaving excess cash in working capital is that it distorts the relationship between working capital and the sales it supports.

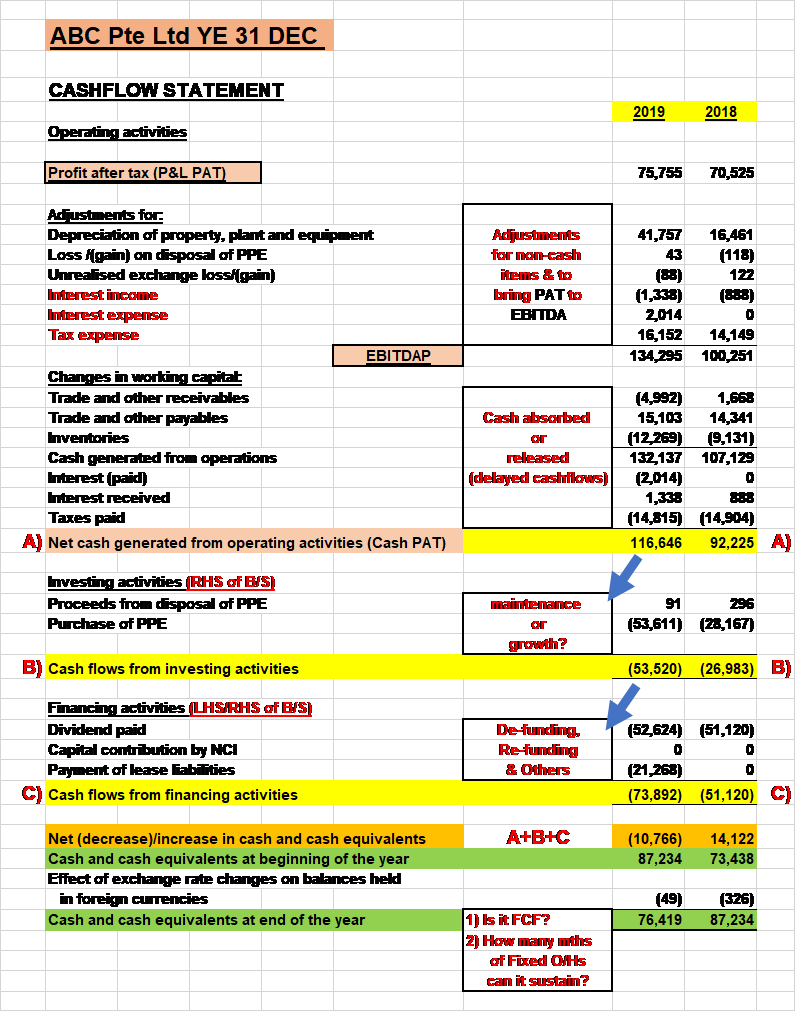

d. CFS presentation – no emphasis on cash PAT

The current CFS allows for variations in presentation. It can start off with PAT or PBT (profit before tax) and treat interest income as an investment activity or an operating activity. This is because the presentation focus is on operating activities and not on PAT (the full P&L).

Business managers would want to know exactly the cash component in PAT realising is that P&L PAT is not fully in cash since some sales, cost and expenses are on credit (delayed cashflows). This is not readily discernible in the current presentation.

e. How do the 3 financial statement link, resource-wise?

Central to the linkage is the CFS. Unless and until the CFS presentation allows for that linkage, there is no way a business manager can figure out how cash and cashflows are generated, properly managed, and appropriately allocated resource-wise.

4. What needs to be done?

a) BS resource presentation

What the entity owes are funding resources acquired at a cost, and it does not include AP, which is part and parcel of working capital, secured at no cost. These funding resources are allocated in the purchase of Property, Plant & Equipment (PPE), to fund investments (such as acquisitions, etc) and working capital. I would call these allocated resources “operating & non-operating resources” or simply “operating resources”.

b).Cash balances – separate line and in currency

Business managers need to know more about the cash balances in the BS,

- What is the cash required for operations and what are in excess of operating requirements?

- Is cash (those in foreign currency) impaired?

- What is the intended use of the excess cash?

A proposed presentation is as depicted. It could be presented in the Notes to Accounts or only in management accounts (if unduly sensitive).

| Current assets | |||||

| Cash and cash equivalents | |||||

| S$ | xxx | ||||

| US$ (rate 1.33) | xxx | ||||

| MR (rate 0.33) | xxx | ||||

| Others | xx | xxx | |||

| Working capital investment | |||||

| Cash and cash equivalents | xxx | ||||

| Trade & other receivables | xxx | ||||

| Inventory | xx | ||||

| Trade & other payables | (xxx) | xxx | |||

| Total current assets | xxx | ||||

c) Allocation of resources (in percentages)

Under the ERAA BS presentation, it is clear how funding resources are allocated to operating resources. These allocations could be presented in Notes to Accounts. In the next period, the allocation may be decidedly different, due to earlier performance concerns when WARA (weighted average return on assets) was not acceptably better than WACC (weighted average cost of capital).

d) P &L presentation – EBITDA to be highlighted

As cash is a critical resource it must be highlighted in the P&L as follows:

Operating profit before depreciation (EBITDA) xxx

Depreciation /Amortisation xx

Operating profit after depreciation (EBIT) xxx

Although EBITDA (Earnings Before Interest, Tax, Depreciation & Amortisation) is not 100% cash, it approximates cash as

- The significant non-cash items of Depreciation and Amortisation are already excluded, and

- Over the next few month after BS date all the delayed cash for the period should be released back to cash.

Business managers would also like to know how much of P&L PAT is in cash. This piece of information cannot be easily presented in the P&L but the CFS could be adjusted to make this information readily accessible.

e) CFS presentation

As discussed in my earlier papers (my Articles 8 & 9), the current CFS presentation allows choices in the treatment of interest expenses and interest income, among other items. The reason is that there is no clear guideline in defining “Cashflows from operating activities”. And therefore, CFS could begin with Profit after tax (PAT) or Profit before tax (PBT).

From the commercial or business point of view, business leaders would like to know what the cash component in PAT is, knowing full well that PAT includes non-cash items and delayed cashflows from working capital items. They also need to clearly see PAT from the Profit & Loss Statement continuing into the CFS to arrive at Cash PAT. So, the starting point in the CFS must be PAT and not PBT.

*

f) Notes to accounts or management accounts

The Notes to Accounts (or in management accounts, if details are highly sensitive) over a 3-year basis should show

- percentage allocation of funding resources to operating resources

- WARA for each year compared with respective WACC. This gives an early warning signal of going concern issues, if any.

- EBITDA/average working capital trend (a leading indicator) over the same period. This indicates how well the company is managing its working capital relative to cashflow generated over the period. There are numerator factors and denominator factors in this indicator that must be analysed and investigated.

5. Conclusion

Professional awakening, recognition and full awareness of this issue are necessary for a focussed action towards ERAA, internationally. Otherwise, business managers remain at best, inadequately enlightened, or at worst, consistently unenlightened in still fully embracing the Entity Approach to Accounting!

Copyright 3rd Jan 2021 Michael M Lee

Note: The new ideas, principles, and concepts presented in this paper are the author’s own and do not represent those of any institution or organisation.

Any Accounting & Finance professionals or institutions who are interested to pursue this ERAA concept/proposal further may write to Michael M Lee at mtclee@singnet.com.sg.

About Michael Matthew Lee

Michael M Lee is a trained teacher, lecturer, coach and facilitator, and is himself a life-long learner. He is currently pursuing the Chartered Valuer & Appraiser Programme at Nanyang Business School.

As a certified trained and facilitator, he is skilful in explaining difficult concepts in a simple and understandable manner. With his more than 40 years of corporate working experience, which include serving as Group CFO of 3 large Main Board public-listed groups, and as MD/CEO/COO of various companies across industries, he specialises in Finance and Strategic Marketing, and is exposed to senior executive management practices, issues and challenges. He adopts a practical approach to his training, facilitation, and consultancy.

Michael is founder and director of The CFO Desk Pte Ltd, a company engaged in corporate training & seminars, financial consultancy (corporate restructuring, IPO advisory, cashflow management), and business valuation.

Michael M Lee’s credentials are:

MBA (Finance, NUS Business School)

MBA (Strategic Marketing, University of Hull)

BAcc (NUS); DipM (UK);; PDipM (APAC); ACTA; PMC

ASEAN CPA; FCA(Singapore); FCPA(Aust); FCCA(UK); FCIM(UK); MSID.

Note:

Michael has already written 9 other accounting & finance articles to-date and they can be accessed at

Website: www.cfodesk.com.sg;

LinkedIn: “Michael M Lee”; and

Facebook: “Michael M Lee”

- 8 Oct 2018: “Debit & Credit” – Upon this Rock, the House of Accountancy was built!

- 17 Oct 2018: Financial Statement Analysis (an overview) – moving from lagging (historical) indicators to leading (predictive) indicators.

- 26 Nov 2018: Traditional Financial Statement Analysis –using lagging indicators (Part 1)

- 17 Dec 2018: Financial Statement Analysis – using leading indicators (Part 2)

- 24 Jan 2019: Financial Statement Analysis –Is there an optimal capital structure? (Part 3)

- 24 Feb 19: Financial Statement Analysis – What is V.I.S.A.? (Part 4)

- 7 Apr 19: Financial Statement Analysis – The V.I.S.A. Approach (Part 5)

- 26 Apr 20: Cashflow Statement – an enhanced presentation

- 28 Jun20: Cashflow Statement – Period & Trend Analysis

————————————————END 3Feb2021——————————————–