Our Articles

The 3 huge unresolved gaps in Accounting & Finance and Operations Management.

10 Dec, by Michael M Lee

Acquisition Appraisal – The M&A IRR Test

16 May, by Michael M Lee

Currently the appraisal of the target is based on many factors which are not known immediately. We need a metric to enable us to decide very quickly whether the target is worth pursuing. We must then know upfront the “return on investment” or IRR (Internal rate of return) on the acquisition (its purchase price) and how much it is below the bidder’s hurdle rate (WACC - Weighted Average Cost of Capital). So, to compute the acquisition‘s IRR, we must turn the acquisition exercise into an investment appraisal exercise. There are reasons why currently this important aspect of M&A deals cannot be done. It is simply because M&A deals do not and cannot easily provide the data necessary to compute IRR. To enable an Acquisition Appraisal to be performed, I have developed "The M&A IRR Test", which will determine to what extent the acquisition IRR is below the hurdle rate, and whether that gap is manageable and acceptable under the bidder's financial policy.

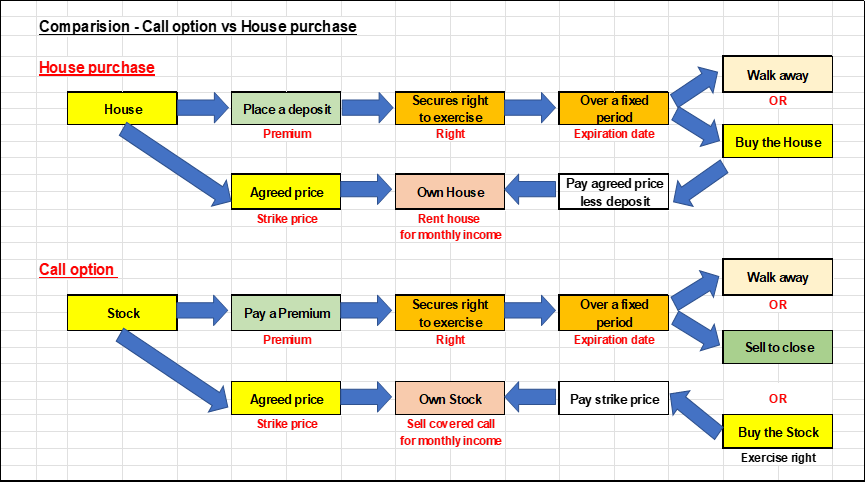

Stock options trading & investment : The Greeks.

17 Nov, by Michael M Lee

Embarking on option trading and investment is not an easy endeavour. It requires knowledge of how option pricing works, how option prices behave, and the parameters which affect option prices, chief of which are the Greeks. Without the use of the Greeks to guide risk management, the trader or investor may not know what to do when option prices collapse or do not move in the direction as expected.

Stock options trading & investment – An introduction

05 Dec, by Michael M Lee

In Rich Dad advisor Andy Tanner’s book “Stock Market Cashflow” on page 220 “How Warren Buffet generates huge profits with options”, Andy wrote, “Buffet sells a lot of options. Why? Because he understands how time decay works to the benefit of the option seller. Options provide him with a great tool to generate additional income for his holding company.” Thus, options can be used to generate additional income. It can also be used for hedging and speculation.

Corporate Cashflow Sustainability – The Foundation for Corporate Growth

24 Sep, by Michael M Lee

Current accounting & finance theory and practice emphasise only on cashflow projections to determine the cashflow health of the company. This is inadequate as it is short-term in nature and by design. We need an assurance how cashflows will behave beyond the projection period ie the company’s Cashflow Sustainability. We are not able to ascertain Cashflow Sustainability because we currently do not have the tools to enable it. We are in a paradigm which is based on the entity concept and financial analysis is based largely on financial ratios which uncover what have gone wrong. They are lagging (historical) indicators! To enable Cashflow Sustainability we need a paradigm shift. We need a) To understand the flow of economic resources through the company and over long periods of time. b) To create new tools which forewarn what could go wrong. These are leading (predictive) indicators. c) To build a Cashflow Sustainability Framework and monitor it, and d) To assess the presence of Cashflow Sustainability periodically.

Business Valuation – Income Approach

07 May, by Michael M Lee

The Income Approach is by far the most rigorous. But there are computation/technical difficulties in this approach which this article addresses. These are: a) What is the key concept in the income approach? b) What is the method of computation of business value using income approach? c) Understanding the 2-part cashflows (5-year explicit forecast period and terminal value period) to be applied in the approach. d) Determination of the discount rate or adjusted WACC e) The perpetuity factor and the Gordon Model f) Understanding Enterprise Value derived from the Income Approach g) Deriving Equity Value (EqV) from Enterprise Value (EV) h) Sensitivity Analysis/Financial Modelling to arrive at an appropriate range of values. i) Counter-check range of values using the multiple-based or other approaches and reconcile the differences. It must be recognised that as Business Valuation is more an art than a science, no two valuations based on the same approach can produce the same outcomes. But the 2 ranges of values can be reconciled based on assumptions applied, the risk assessment of the valuation, the availability of the information provided by client or extracted from public sources, the defensibility of the figures, and how each valuer exercises his/her judgement and effort in maximising the range of value defensibly for the client.

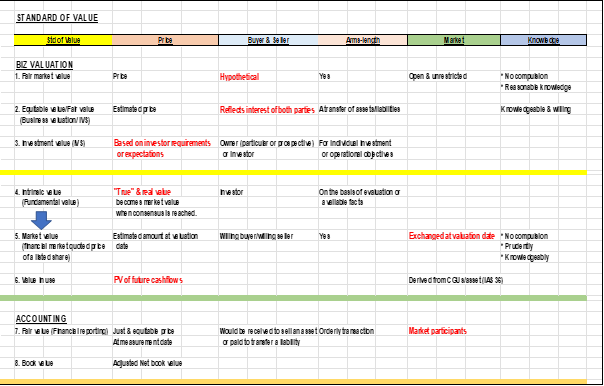

Business Valuation – A primer

20 Apr, by Michael M Lee

Business Valuation is a relatively new profession and is an area where certain accounting standards and principles may not readily apply. As it is more art than science, it is incumbent on the valuer to apply his/her expertise, experience, knowledge, and competence to determine, defend and maximise the value of subject matter assigned.

The Essence of Corporate Cashflow Sustainability

26 Jan, by Michael M Lee

"The Essence of Corporate Cashflow Sustainability' is my first Finance book published in early June 2022 for both local and international readership. It is not an academic treatise but one written based on my decades of corporate experience both at the Finance and Operations senior executive levels. This book explains how you can develop, build, monitor and assess Cashflow Sustainability (in a Framework) for your company to support ongoing corporate growth. It is both enlightening and career-enhancing as the knowledge and skillsets to be acquired from this book are not available in current Finance textbooks/literature; much less from practice. The synopsis, outline and preface of the book as well as the book testimonials can be found in the main text. Please do not hesitate to contact me at michael@cfodesk.com.sg if you need further information.

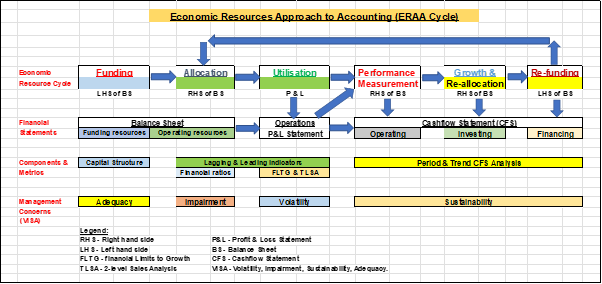

The Economic Resources Approach to Accounting (ERAA)

05 Feb, by Michael M Lee

Traditional accounting embraces the entity concept, which is good for explaining debits & credits, and what the entity owns and owes. But as businesses evolve, sustainability of cash and cashflows becomes vital, while the emphasis on entity and its going concern assumption remains important. Without cash and cashflows there is no entity, let alone going concern! Most companies painfully experience this situation during the current world-wide pandemic! Cash is the most vital economic resource for an entity‘s survival and so my proposed new concept and approach is called “The Economic Resources Approach to Accounting” (ERAA), shifting the focus from Entity to Economic Resources. The business owner, the Board and Management’s main interest is on how the economic resources of the company are acquired, allocated/deployed, profitably utilised, and redeployed. The current set of financial statements do not reflect this economic cycle clearly. For centuries, Accounting has been entrapped by the Entity focus, losing sight of the greater importance of Economic Resources. My article on ERAA (as attached) highlights this issue and proposes solutions. Professional awakening, recognition, and full awareness of this issue are necessary for a focussed action towards ERAA, internationally. Otherwise, business managers remain at best, inadequately enlightened, or at worst, consistently unenlightened in still fully embracing the Entity Approach to Accounting!

Cashflow Statement – Period & Trend Analysis

29 Jun, by Michael M Lee

Cashflow Statement – Period & Trend Analysis This is follow-on paper of my earlier paper dtd 26 April 2020 on “Cashflow Statement (CFS) – An enhanced presentation”. In this paper, which is geared towards the business leaders’ perspective, I shall discuss 1) Why a company’s sustainability of cashflow is important 2) The current CFS presentation allowing for different treatment of certain items 3) The traditional way of analysing Period CFS, and a proposal for a robust approach 4) Trend CFS analysis, leading to the determination of the company’s cashflow sustainability, and how the finance leader needs to be involved in strategic thinking process to assess whether investment activities are appropriate for maintenance or corporate growth per strategic plan. The business community needs to know that cashflow sustainability of a company is a necessary but not sufficient condition for the company’s overall financial health. The company also needs to grow its operating resources to further validate its going concern assumption.

Cashflow Statement – An Enhanced Presentation

26 Apr, by Michael M Lee

The Cashflow Statement is the most important period statement as it depicts the cashflow health of the company. In its current presentation format, it may not be as useful as it should be, especially for non-accounting trained users who may be Board directors, Senior Management, shareholders or investors. These business readers/users are interested to know:. a) Why P&L Profit after tax (PAT)is not all cash?, b) What is the fully cash PAT?, c) What cause an adverse Cashflow Gap between P&L PAT and fully cash PAT and how can it be fixed?, d) Is the company’s going concern assumption threatened as a consequence of a huge negative Cashflow Gap? Unfortunately, the current presentation format does not highlight these areas simply because the focus is not on the PAT Cashflow Gap!

Financial Statement Analysis – The VISA Approach (Using both leading and lagging indicators) (Final Part 5)

31 Jan, by Michael M Lee

Central to the V.I.S.A. Approach is the appreciation of the economic flows of transactions through the accounting system as depicted in the ERAA diagram. Then the key factors (V.I.S.A. components) in each of the financial statements, which pose potential risks to the financial health of the company must be recognised. Reviewing and analysing these key factors using both lagging and leading indicators on a regular basis (quarterly) and taking the appropriate actions to mitigate or forestall the risks will save the company from unintended corporate failure.

Financial Statement Analysis – What is V.I.S.A.? (Part 4)

31 Jan, by Michael M Lee

In this penultimate part of my 5-part series on Financial Statement Analysis (moving from lagging to leading indicators), I shall discuss the areas in the financial statements (Balance Sheet, P&L Statement, and Cashflow Statement) in which accountants/CFOs and CEOs are seriously concerned about, agonising over the sustainability of the firm’s operational and financial performance. This is more so when the firm’s business or the economy heads south.

Financial Statement Analysis – Is there an optimal capital structure? (Part 3)

31 Jan, by Michael M Lee

This is the 3rd accounting & finance article of my 5-Part Financial Statement Analysis (FSA) series. In this article, I shall discuss capital structure; its importance and implications to financial management and operational success. Much of the discussion will be centered on the practical aspects rather than its theoretical underpinnings (ie setting aside Modigliani & Miller Theorem and Robert Hamada’s Equation).

Financial Statement Analysis – Using leading indicators (Part 2)

31 Jan, by Michael M Lee

This is the second of my 5-article series on the inadequacy of traditional financial statement analysis (FSA) in predicting, preventing and protecting business and financial risks of a company. The following 2 leading indicators are useful in managing such risks.

Financial Statement Analysis – Using lagging indicators (Part 1)

01 Jan, by Michael M Lee

his article is the first of 5 parts which examine why traditional financial statement analysis (FSA) using ratios are lagging in the prediction, monitoring and control of the financial health of a company. It ends with how a systematic and integrated approach applying both lagging and leading indicators could proactively satisfy those objectives.

Financial Statement Analysis – Moving from lagging to leading indicators

15 Nov, by Michael M Lee

Every accountant is expected to know how to perform a Financial Statement Analysis, which is key to understanding the financial health of any company. However, traditional financial statement analysis uses financial ratios which are based on historical (after-the fact) data. They produce an analysis which, at best, are lagging indicators of the financial health of a company.

“Debit and Credit” – Upon this Rock, the House of Accountancy was built!

14 Nov, by Michael M Lee

While debits and credits appear basic and simple to the accountant, their explanation and determination are not. This paper provides the explanation and guidelines in treating the 2 legs of a transaction as debit or credit. I hope it now makes good sense in rationalizing what appears to be “mysterious” to non-accountants and accountants alike.