The 3 huge unresolved gaps in Accounting & Finance and Operations Management.

10 Dec, by

Article 17 – The 3 huge unresolved gaps in Accounting & Finance and Operations Management.

By Michael Matthew Lee (3rd Dec 2024)

- Introduction

In the world of accounting and finance and corporate executive management and operations, they are three huge unresolved gaps which, over the years, have caused big and small companies alike to fail. Unfortunately, most of these failed companies do not know what hit them devastatingly!

With more than 40 years of corporate experience as Group CFO in three large main board public-listed companies in Singapore and as Managing Director/CEO of companies in the automobile, food and food processing, and telecommunications industries I realize that the three huge gaps are:

a) The lack of knowledge and implementation of cashflow sustainability in the company to enable and support corporate growth continuously.

b). The absence of a proper definition for corporate growth, and how to execute it and assess its outcome.

c). For M&A activities, the absence of a critical measure to determine upfront whether it is worthwhile to continue to pursue the target. This would save hefty overpayment for the acquisition, resulting in subsequent impairment losses.

- Cashflow sustainability

Currently a company’s cashflow health is predicated on the accountant’s three-year or five-year cashflow projections based on reasonable assumptions of sales collections, payments, cost, and expenses. Whether there will be cashflows to support business growth beyond the projection period is largely unknown. This does not augur well for the company which requires adequate cashflows to fund its businesses indefinitely.

This situation arises because accounting and finance (A&F) and marketing, sales and operations (MSO) are distinct and separate disciplines. And top management of each discipline do not normally cross borders! But for cashflow sustainability to exist, both A&F and MSO must work together as the cashflow engines in each discipline must “feed” each other.

Recognizing this issue, I have created the financial and operational tools and the framework necessary to develop cashflow sustainability. This “thesis” is promulgated in my first book entitled “The Essence of Corporate Cashflow Sustainability”. You are advised to read this book thoroughly to enable you develop a cashflow sustainability framework for your company.

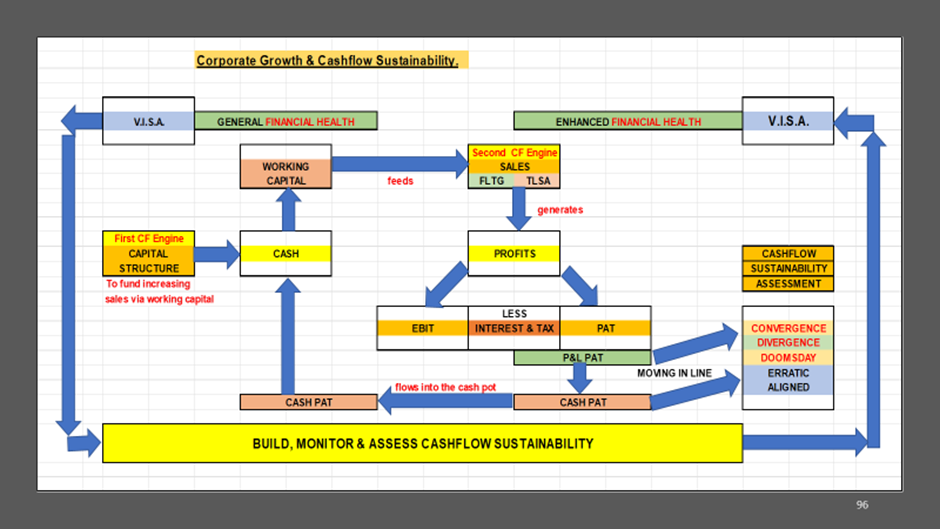

Figure 1 delineates the Cashflow Sustainability Framework, which starts with assessing the current financial health of the company using lagging indicators or traditional financial ratios. The Framework emphasises 3 important aspects, namely

- a) The cashflow engines – capital structure and sales,

- b) The economic resources approach to accounting (ERAA), and

- c) The assessment of the presence of cashflow sustainability

Figure 1: Cashflow Sustainability Framework

Figure 1: Cashflow Sustainability Framework

2.1 The cashflow engines – capital structure and sales

Every company has 2 cashflow engines viz capital structure (the cashflow funding engine) and sales (the cashflow generating engine). The capital structure comprises equity (shareholders’ funds) and debt (bank long term borrowings). Each has a cost and equity funding is more costly because they do not have security over the company’s assets.

The weightage of each funding is also critical as more equity funding would result in a higher Weighted Average Cost of Capital (WACC). The assets (fixed assets, long-term investments, working capital investment) acquired from these funds would be at the WACC rate. Therefore, the cash balances in working capital is also at WACC rate, not at the bank borrowing rate! When cash is used to purchase another factory equipment to increase production and subsequently sales, the new factory plant must provide a return on investment (the IRR or internal rate of rate) higher than the WACC rate. We call this rate on the asset side, the “hurdle rate”. And IRR of the new factory plant must jump over the hurdle rate (or WACC rate). If IRR is lower than the hurdle rate, the new investment cannot be accepted as it would result in shareholder value erosion! This affects the corporate growth of the company and so the capital structure must be properly managed to ensure that WACC (and subsequently hurdle rate) is not unreasonably high.

On the MSO side, Sales is the cashflow generating engine. This engine must be protected, enhanced and grow. There is a tendency for the CEO to stretch sales beyond the limit of existing financial resources, typically working capital. The Financial Limits to growth (FLTG) and Two-Level Sales analysis (TLSA) are two important leading indicators to ensure guard-rails are in place and that management is aware of the impending dangers to sales growth on the horizon.

Obviously, both A&F and MSO must work closely to ensure that the 2 critical cashflow engines support and “feed” each other.

2.2 The economic resources approach to accounting (ERAA)

ERAA refers to the flow of economic resources through the accounting system and at critical junctures, we must determine if the economic flows are adequately and appropriately applied and re-applied to ensure corporate growth and profitable outcomes.

Figure 2 depicts the economic resources flow starting from equity and debt funding (right hand side of Balance Sheet) to their allocation to fixed assets, long-term investments, and working capital investments (right-hand side of Balance Sheet).For allocation to be appropriate, we must ensure that the proportion of allocation must be defensible. If there is unduly heavy allocation in long-term investments in associated companies and joint ventures, both of which the company has no financial and operational control over, the company may suffer from wrong decisions made in those companies.

Figure 2: Economic Resources Approach to Accounting (ERAA)

The economic flows continue into operations and its results must show sales growth and earnings profitability. Otherwise, a re-allocation of resources at the assets end is needed. The cashflow statement provides clarity on the operational results, cashflow-wise, and this would determine total assets re-allocation and additional funding requirements, or funding reduction.

The metrics section shows the key measures needed to examine the performance at each critical juncture of the economic resources flow.

As cashflow sustainability requires a good management of economic resources flows, the ERAA Framework is set up to perform this task.

2.3 The assessment of cashflow sustainability

My first finance book “The Essence of Corporate Cashflow Sustainability” details the set up of a Cashflow Sustainability Framework (CFSF), which encompasses the management of the 2 cashflow engines and the ERAA sub-framework.

To ensure that the CFSF is operating effectively, we must assess it on a quarterly (or yearly) basis and enhance it appropriately.

As illustrative, we show 5 companies with their respective P&L PAT and Cash PAT over 3 years (Figure 3.1). The 3-year trend is a leading indicator as it shows a pattern of behaviour that allows the analyst to project its future trend. A diagrammatic presentation of each company’s trend lines is shown in Figure 3.2.

| Company | P&L PAT ($’000) | Cash PAT ($’000) | ||||||

| 20X1 | 20X2 | 20X3 | 20X1 | 20X2 | 20X3 | |||

| ABC | 20 | 10 | 5 | 25 | 35 | 40 | ||

| DEF | 5 | 10 | 20 | 35 | 30 | 25 | ||

| GHI | 20 | 15 | 5 | 35 | 30 | 25 | ||

| MNO | 10 | 20 | 5 | 40 | 25 | 30 | ||

| PQR | 10 | 15 | 25 | 30 | 35 | 40 | ||

Figure 3.1: P&L PAT and Cash PAT data

Figure 3.2: P&L PAT and Cash PAT scenarios

The essence of cashflow sustainability is for the trend P&L PAT and the trend Cash PAT to feed each other. The diagrams show that divergent, convergent and doomsday scenarios lack cashflow sustainability, while in erratic and aligned scenarios cashflow sustainability exists.

There are 3 caveats in this illustration.

- Unless a CFSF is set up in the company, a seemingly erratic or aligned scenario is not conclusive of cashflow sustainability.

- In an erratic scenario, a third point to the left is needed. This is to show whether there is a likely trend reversal in one of the 2 trends.

- For the first 3 scenarios, it is necessary to review the downward trend lines and take corrective/remedial actions.

This paper only highlights the unresolved gaps and the solutions. You are advised to read the book for a full discourse on this subject.

Kinokuniya (Orchard) Singapore weblink for book order:

https://singapore.kinokuniya.com/The_Essence_of_Corporate_Cashflow_Sustainability/bw/9789811837784

- Corporate growth

For a company to be able to grow its businesses and expand its operations into the future, a clear definition of corporate growth is required. The definition must encompass the ingredients of corporate growth, and how they are developed and measured. Without measurement, the company just drifts along and subsequently fails.

My second book, entitled “Corporate Growth, and Cashflow Sustainability” clearly defines what corporate growth is and how it is to be developed through organic and non-organic growth. This growth must be underpinned by a cashflow sustainability framework discussed in my first book. I have promulgated that the final test for corporate growth is to analyze the three-year growth trend of total assets. But the ultimate test should be the growth of the company’s equity value (Figure 2.1). You are also advised to read this book to fully appreciate the importance of the health of the company’s ecosystem and execute appropriate strategies for ultimate growth in your company’s equity value.

In current A&F books and literature, corporate growth is not defined. But yet corporate growth is the life-line for a company to survive to eternity! The closest discourse on this topic is strategic marketing management, which only emphasises on the MSO domain and nothing on how strategies affect the A&F domain. So, the CEO is driven to aggressively increase sales, cut costs and expenses, and watch EBIT and earnings grow; only to ultimately collapse under the weight of operating beyond the company’s financial limits to growth!

My solution to this knowledge and application gap is to critically define corporate growth both from the A&F domain (growth in sales, earnings, and total assets; and cashflow sustainability) and the MSO domain (organic and non-organic growth and shareholders’ value (equity value)). Ultimately, it is the growth in equity value that matters most!

Figure 2.1 Corporate Growth Framework

You are advised to read the book ‘Corporate Growth & Cashflow Sustainability” for a full discourse on this subject.

Kinokuniya (Orchard) Singapore weblink for book order:

Books Kinokuniya: Corporate Growth & Cashflow Sustainability / Lee, Michael Matthew (9789811886102)

- M&A IRR upfront measure

There is always a tendency for merger and acquisition targets to be acquired at a hefty price. This results mainly from impairment losses a year after acquisition. This would not have happened if we have an M&A metric upfront that could help us determine whether to continue negotiating with the target or walk away. My thoughts in this area centre around using a metric such as IRR (Internal Rate of Return) to determine whether the gap between this IRR and the hurdle rate (WACC) can be managed after acquisition. This is akin to an investment appraisal exercise whereby the IRR of the investment must be above the hurdle rate to be acceptable. In the M&A situation, the IRR will always be below the hurdle rate because of the “goodwill” element in the purchase price. The key decision is how wide a gap between hurdle rate and M&A IRR can the company accommodate.

- Why is IRR so important is assessing an acquisition purchase price?

In a normal acquisition, we establish the company value of the target. We then work on due diligence to determine the synergies to be extracted from the target (among other considerations and factors) and arrive at defensible purchase price. We then raise funds (either debt or equity or a combination) to effect the acquisition. Let us pause at this point to assess what could go wrong so far.

- The cost of funding is WACC say at 9%, and it sets the hurdle rate to determine if the acquisition provides a return (its IRR) higher than the hurdle rate. Unfortunately, there is no way you can determine the IRR of an acquisition! Why? Because an acquisition deal is not an investment appraisal exercise!

- If we can establish the acquisition‘s IRR, then we will need to know the IRR at 2 points viz. target value and target purchase price.

- We need to know if target value IRR is higher or lower than hurdle rate and to what extent.

- We also need to know to what extent the target purchase price is lower than hurdle rate, knowing full well that there is a “goodwill” element in target purchase price.

- With a good understanding of the 2 IRRs vis-a-vis the hurdle rate, we can assess how well we can close the gap between hurdle rate and IRR of purchase price within one year based on the expected realisation of the identified synergies and implementation of strategic growth decisions in the acquisition.

The crux in this issue is the establishment of the acquisition IRR. And this could be done by turning the acquisition exercise into an investment appraisal exercise. When this is effected, we will be able to make a cogent decision on whether to accept or reject the acquisition and not allow the acquisition to be accepted “blindly” resulting in huge post-acquisition impairment! Currently, we simply assess how much more in percentage terms over its value we are paying for the target and if we are “comfortable” with the percentage, we proceed with the acquisition (among other considerations and factors).

I shall not explain how we can extract an M&A IRR upfront as it is documented in my earlier article on “Acquisition Appraisal – The M&A IRR Test (preventing post-acquisition impairment upfront!)” (Website: https://cfodesk,com.sg/articles).

- What if you need to acquire the target beyond the ‘comfortable” IRR gap?

If for whatever reasons, the target acquisition is necessary for strategic fit and corporate growth, and it is “ordained” by top management, then there is a need to assess whether the potential “fall-out” in subsequent impairment would drag the group profits into a significant loss position. We must compare a reasonable percentage of the “goodwill” payment against the past 3 years average group earnings and assess whether it is within the company’s “pain” threshold.

So long as the subsequent year does not result in a significant group loss, there is still time to recover through strategic initiatives for the target and overall group organic growth.

I shall be embarking on writing my 3rd corporate finance book entitled “The Finance Leader’s Handbook”, which will cover this topic in greater detail.

- Conclusion

The 3 huge unresolved gaps as identified and discussed are not insurmountable. They have been lingering gaps because A&F and MSO are separate and distinct disciplines. Between these 2 domains, barriers and borders must be crossed to ensure a better understanding of each other’s expertise and establish the necessary frameworks and metrics to close these huge gaps for practitioners.

———————————————MMLee 3Dec2024——————————————-

Michael Matthew Lee’s credentials:

Chartered Accountant (ISCA)

Chartered Marketer (CIM(UK))

Associate CVA (SAC-IVAS)

MBA (Finance, NUS Business School)

MBA (Strategic Marketing, University of Hull)

BAcc (NUS); DipM (UK); PDipM (APAC); ACTA; AWP, CertEd

ASEAN CPA; FCA(Singapore); FCPA(Aust); FCCA(UK); FCIM(UK); MSID.

————————————————————————————————————–